")

Hello Finance Enthusiasts!

Today we delve into a topic that is often at the center of heated debate and political debate: the debt ceiling. You may have heard this term thrown around, but do you really understand what it means and why it is important to your personal finances? We are here to demystify that mystery and reveal how the debt ceiling could affect your financial future.

What the debt ceiling is and why it matters

Debt ceilings are at the heart of it teeth A legal limit on the amount of debt a government can accumulate to finance its operations and meet its financial obligations. Think of this as a fiscal cap that limits the government’s ability to borrow. At this point, you may be asking, “Why should I care about the government debt ceiling?” Well, my friends, the answer lies in the ripple effect it has on various aspects of the economy and ultimately personal finances.

Reaching the debt ceiling triggers a delicate dance of political negotiations and potential outcomes. Failure to raise the debt ceiling could lead to government shutdowns and defaults on fiscal debt. This scenario could severely impact the economy, causing financial market instability, interest rate rises and currency depreciation. And what do you think? All these factors can directly affect your wallet.

What happens if the debt ceiling is raised (or not raised)

If the government raises the debt ceiling, it will be able to continue borrowing and meet its fiscal obligations. This measure will provide stability and ensure the functioning of critical government services. But it also means that government debt burdens continue to grow, and the long-term implications may be worrisome.

On the one hand, failure to raise the debt ceiling could lead to government shutdowns or, worse, default on debt payments. This could cause a domino effect, causing panic in financial markets, increasing borrowing costs and leading to a recession. These conditions affect business, job security and overall consumer confidence, and have a direct impact on economic well-being.

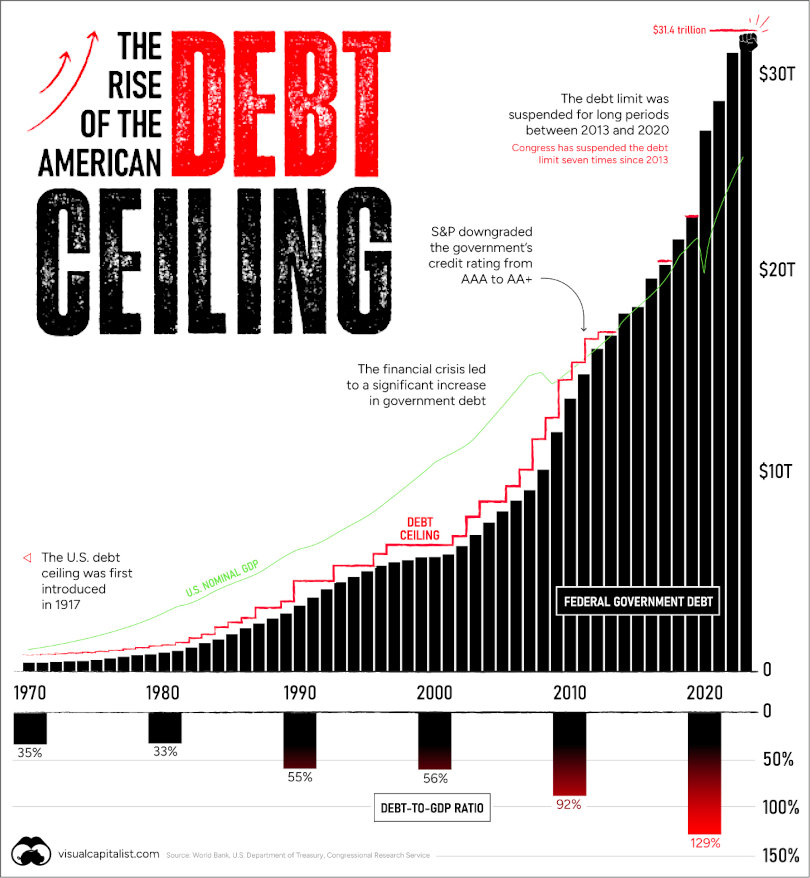

So what ceiling height are we talking about?To give you some ideas, here it is list The last five US debt ceiling hikes and their amounts:

- September 28, 2017: Increased by $1.5 trillion to $20.3 trillion.

- August 1, 2019: $22.3 trillion, an increase of $2 trillion.

- December 21, 2020: increased by $480 billion to $22.78 trillion.

- August 11, 2021: $26.28 trillion, an increase of $3.5 trillion.

- March 15, 2022: $30.78 trillion, an increase of $480 billion.

June 1, 2023 deadline to raise federal debt ceiling approaches caused concern As US Treasury Secretary Janet Yellen warned that the government is incapable of paying all bills. President Joe Biden, while not accepting the Republican proposal, remains open to spending cuts and tax adjustments in preparation for a potential deal.

Failure to raise the debt ceiling could trigger financial market turmoil and interest rate hikes, highlighting the need for urgent action to avoid a potential default and its far-reaching consequences.

How to respond to government decisions on debt ceilings

As individuals, it is imperative to be proactive in preparing for a possible government decision on the debt ceiling. Here are some steps you can take to protect your personal finances.

- Stay up to date with: Stay tuned for news and updates on the debt ceiling. Understand the potential impact and how it might affect your financial situation.

- Budget and save: Set a solid budget and set aside an emergency fund. Having a financial safety net can help you navigate uncertain times and unexpected economic fluctuations.

- Diversify your investments: Consider diversifying your investment portfolio to spread your risk. Consider different asset classes such as stocks, bonds, real estate, and commodities to protect yourself from potential market volatility.

- Minimize Debt: Control personal debt. When the economy becomes unstable, high-interest debt can become a burden. Prioritize paying off your debts and avoid unnecessary financial obligations.

- Seek professional advice: Talk to a financial advisor to assess your personal situation and develop a customized plan. They can provide guidance on how to navigate uncertain financial situations and make informed decisions.

![]()

Conclusion

Understanding the debt ceiling and its impact on personal finances is very important for all of us. As citizens, it is imperative that we stay informed, prepared, and take necessary steps to protect our economic health. By acting proactively, budgeting wisely, and diversifying our investments, we can navigate uncertain waters and protect our personal finances from the potential impact of debt ceiling decisions.

Remember, your financial future is in your hands, and with knowledge of the factors that can affect it, you can make informed decisions. Become.

The debt ceiling may seem like a distant and complicated issue, but its implications can have a big impact on our daily lives. By understanding its importance, you can better anticipate potential challenges and adapt your financial strategy accordingly.

So the next time you hear a debate about the debt ceiling on the news or among your friends, you won’t have to worry about it. You will be able to understand its impact and how it relates to your personal finances.

In a world where economic conditions can change rapidly, it is important to stay informed and prepared. Take control of your financial future by learning about the debt ceiling and its far-reaching implications. In doing so, you will be better prepared to weather the storms that may come and ensure your personal financial stability.

Remember, financial literacy is a lifelong journey, and every step you take to understand complex subjects like the debt ceiling brings you closer to economic empowerment.

Be curious, stay informed, and be proactive in managing your personal finances. The debt ceiling may be a puzzle, but with the right knowledge and mindset, it can pave the way for a secure financial future.

We support your financial well-being and your pursuit of knowledge.