Forty years of history tells us it won’t end until the two-year bond yield overshoots the EFFR. It is down for the first time in a year, and inflation is accelerating again.

Written by Wolf Richter of Wolf Street.

The collapse in energy prices and the decline in durable goods prices caused inflation to fall sharply in 2023, surprising us. Both have come out of the sharp price increases since mid-2022, pushing the overall CPI inflation rate down from 9.0% in June 2022 to 3.1% in January 2024. However, services inflation remained high and accelerated in the second half of 2023, which was not surprising. And on top of this increase, the annual rate jumped by 8.2% in January.

The Producer Price Index (PPI), which indicates inflationary pressures deep in the fabric of the economy, caused another nasty surprise in January, with the Services PPI rising 7.1% annually and the Finished Goods PPI rising 4% annually.

The PCE price index for January has not yet been released, but the PCE price index for core services in December accelerated to an annualized rate of 4.0%. Therefore, given the increase in CPI for core services in January, we can expect another nasty surprise, so to speak, in the core PCE price index for services.

Energy prices will not fall forever. Recently, the prices of crude oil and gasoline have increased. WTI is back to near $80. Furthermore, although prices of durable goods cannot fall forever, given their past high prices, they may continue to decline for some time. If energy and durable goods prices simply stalled, overall inflation would be faster because these two large categories would no longer be a counterweight to services. If energy and durable goods prices start rising again, all bets are off.

Therefore, we are currently considering a scenario in which inflation accelerates again. In a few months’ time, he may look back on 2023 and find it to be another false year, notorious for inflation.

And there are indicators that this may be the case. It is the two-year Treasury yield compared to the effective federal funds rate (EFFR).

Two-year bond yields have not yet overshot.

Two-year Treasury yields typically rise before the Fed starts raising interest rates. They did so in anticipation because the Fed had given advance notice of a rate hike and the market had begun pricing in, if not denying, the rate hike ahead of time. The two-year bond yield is the first to react.

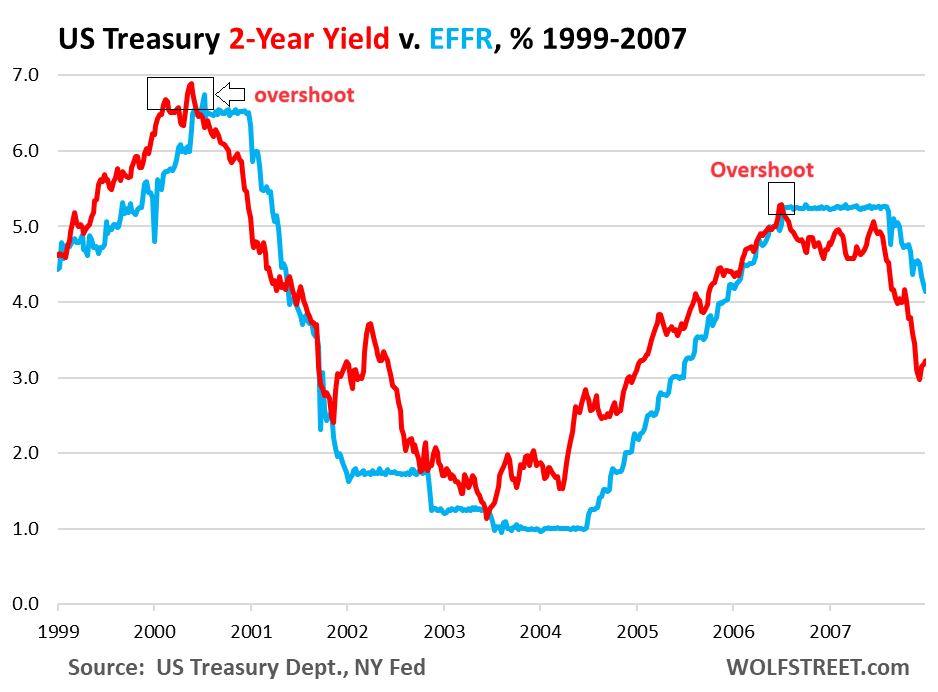

In the current tightening cycle, two-year Treasury yields began rising in October 2021, about five months before the first rate hike. The Bank will continue to anticipate interest rate hikes thereafter. We’ve been doing that for decades. And because it precedes a rate hike, if the Fed stops raising rates, the two-year Treasury yield will overshoot by a small to large amount. While they have overshot every rate hike cycle over the past 40 years, this one is an exception.

However, 2-year yields have been below this cycle.. In November 2022, two-year bond yields are negated and begin to fall, despite the Fed raising rates four more times. By December 2022, when the Fed raised rates, the two-year bond yield (red) fell below EFFR (blue) and has remained below EFFR ever since.

The 2018 interest rate hike caused two-year bond yields to overshoot. Works in the classic way. The Fed last raised interest rates in December, peaking EFFR at about 2.4%. The two-year bond yield was 60 basis points higher, and it paid off.

Clearly, the two-year bond yield is not a do-it-yourself ghost. This is an index that tracks the market for Treasury bills, a huge global market where humans and algos trade and bet. And the typical two-year bond yield overshoot on EFFR was a sign that these guys and the algos were taking the Fed seriously and not blowing it off or denying it.

The fact that the 2-year bond yield has been undershot since December 2022 is a sign that these people and the algos are blowing the Fed away, not taking it seriously, and denying inflation and rate hikes. .

This has surprisingly eased financial conditions, tightening spreads on risky bonds and lowering long-term yields. These easing of financial conditions are part of the driving force currently pushing up inflation.

In the past, it wasn’t over until a fat woman sang..

The Fed is trying to tighten financial conditions in the market by tightening monetary policy, and it is believed that tight financial conditions will make it harder for businesses and consumers to borrow, leading to a slight slowdown in demand. It is thought that it will gradually slow down. By reducing corporate pricing power and making consumers more careful with how they spend their money, inflation should slowly come back into the bottle.

However, by 2023, financial conditions have eased dramatically and inflation is accelerating again.

And the undershoot in the two-year Treasury yield seems to tell us that the long run of rising inflation and interest rates won’t end until the “fat lady” sings. “Fat Woman” sings about the two-year bond yield and when it overshoots. EFFR.

And if it overshoots EFFR, it’s because markets and people are taking the Fed seriously, so monetary conditions are tightening and magic happens on demand. But that didn’t happen this time.

So there is now some suspicion that inflation won’t actually come back into the bottle until the two-year bond yield overshoots the EFFR, allowing monetary conditions to ease significantly and inflation to rise. Therefore, the Fed may need to raise rates further. Then, as EFFR rises, the 2-year bond yield will move backwards instead of forwards, making this whole plan to put inflation back in the bottle much more difficult.

There is another factor here that accelerates inflation. Huge and reckless government deficit spending, with fiscal policy effectively running counter to the Fed’s monetary policy, makes the business of putting inflation back in the bottle even more difficult.

Previous example of a fat woman singing.

In the chart above, we can already see the overshoot of the 2018 rate hike. Here are the last two rate hike cycles: the late 1990s and his 2005-2006. In both cases, the 2-year yield exceeded his EFFR.

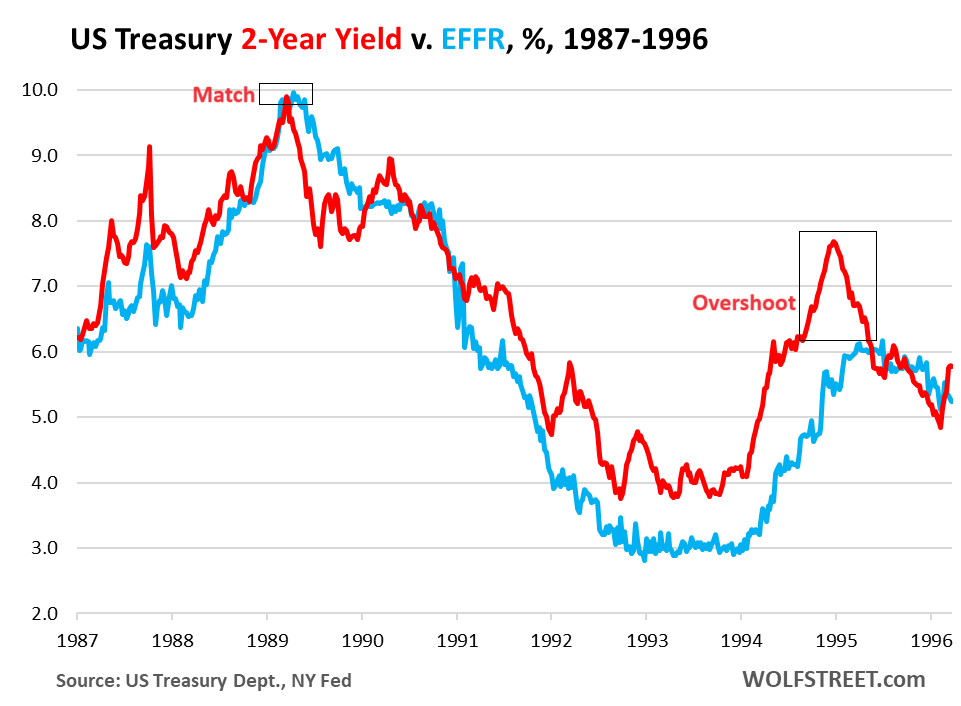

And here we have the 1987-1989 rate hike and the 1994 rate hike. In 1994, the two-year Treasury yield was significantly higher (180 basis points), meaning the market was taking inflation and the Fed very seriously. In 1987, the two-year bond yield also overshot significantly. However, at the peak of the rate hike cycle in 1989, it matched the EFFR at 9.9%.

Do I have to wait until the fat lady sings?

We are not trying to predict where inflation will go. That’s a fool’s errand. But we know what’s happening now. Loose financial conditions are contributing to inflation. Government deficit spending is huge and also fuels inflation. Consumer and business demand is strong, with incomes beginning to rise above CPI inflation in 2023. And there is little other than the Fed’s short-term interest rates putting downward pressure on inflation.

We think inflation and interest rate hikes won’t end until the fat lady sings. And this opera could continue for some time as the market blows the Fed away and the Fed isn’t doing what it wants, which is tightening monetary conditions to rein in inflation.

Enjoy reading and supporting Wolf Street? You can donate. I appreciate it very much. Click on the beer and iced tea mugs to see how.

Would you like to receive email notifications when new articles are published on WOLFSTREET? Sign up here.

![]()

")