Serious talk about 10-year yield and mortgage interest rates

My research on housing focuses on the 10-year yield and the economics that drive it. Looking at year-on-year data, the rate of inflation growth has slowed significantly, but mortgage interest rates have not. This is not surprising, since my beliefs are: “Labour over inflation.”

The 10-year bond yield in 2024 is 3.80%-4.25% As long as the economic data is strong and the Fed doesn’t change direction, it looks perfectly normal to me.I can’t see the 10-year yield below. 3.37% Unless the labor market collapses, the four-week rolling average of jobless claims will exceed 323,000. This means that until the labor market and economy weaken, it’s hard to imagine mortgage rates falling below 6%, especially with tight spreads.

But it’s now at the same level as last year, near the important 4.34% level, with the Federal Reserve on the horizon. As you can see from the graph below, this is a big week.

With mortgage rates once again above 7%, this meeting comes as the Fed has made clear over the past few meetings that policy has been restrained and does not want to become too restrictive. We’ll have to wait and see what the Fed says. This is what happened last year when the 10-year Treasury yield was heading towards 5% and mortgage rates were 8%. However, there is a risk that the Fed may appear too hawkish again, pushing 10-year Treasury yields higher.

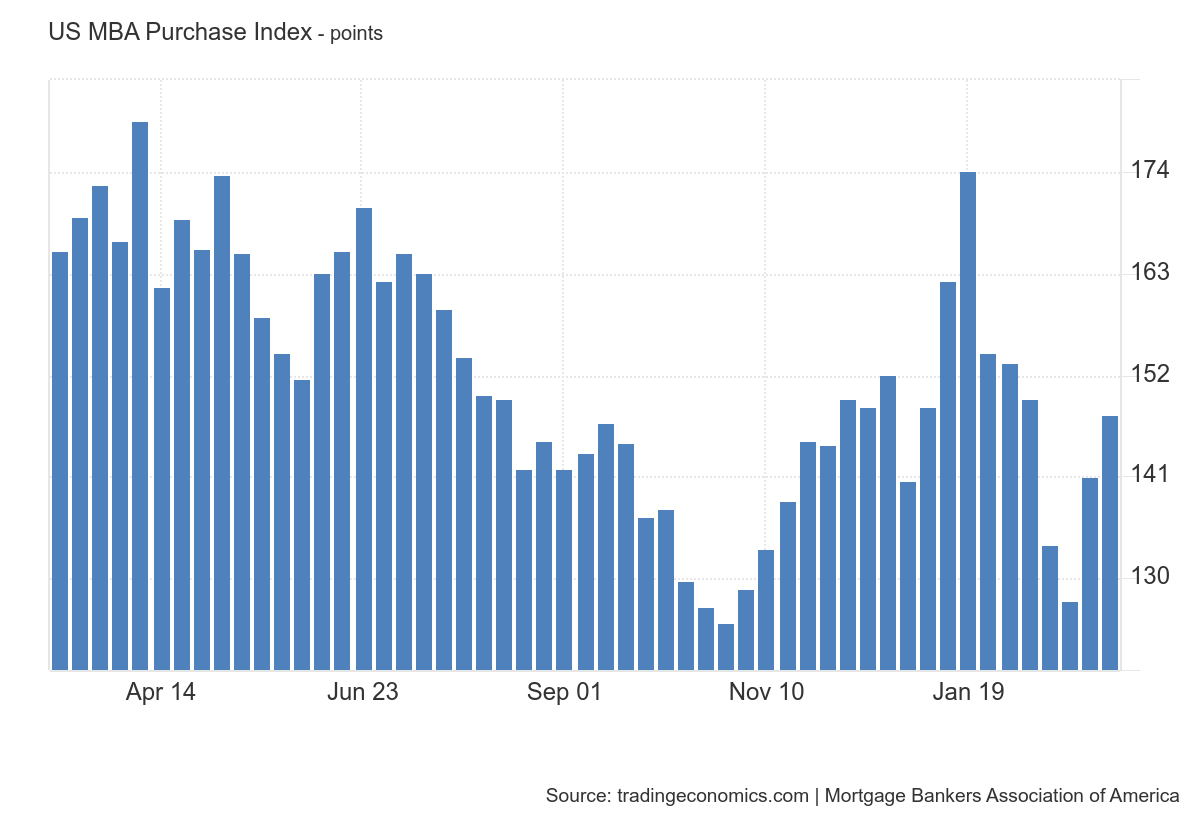

Purchase application data

With mortgage rates falling recently, purchase application data has increased for several weeks in a row, which is consistent with last year’s situation. Since we are working from a very low level on this data line, the bar is so low that it won’t take much to move the needle.

Since November 2023, there have been 10 positive purchase applications and 5 negative purchase applications after adjusting for holidays. From the beginning of the year to now, there have been 4 positive prints and 5 negative prints. It’s clear that demand will increase if mortgage rates head toward 6% and stay there, but more people buying homes will keep the Federal Reserve up at night.

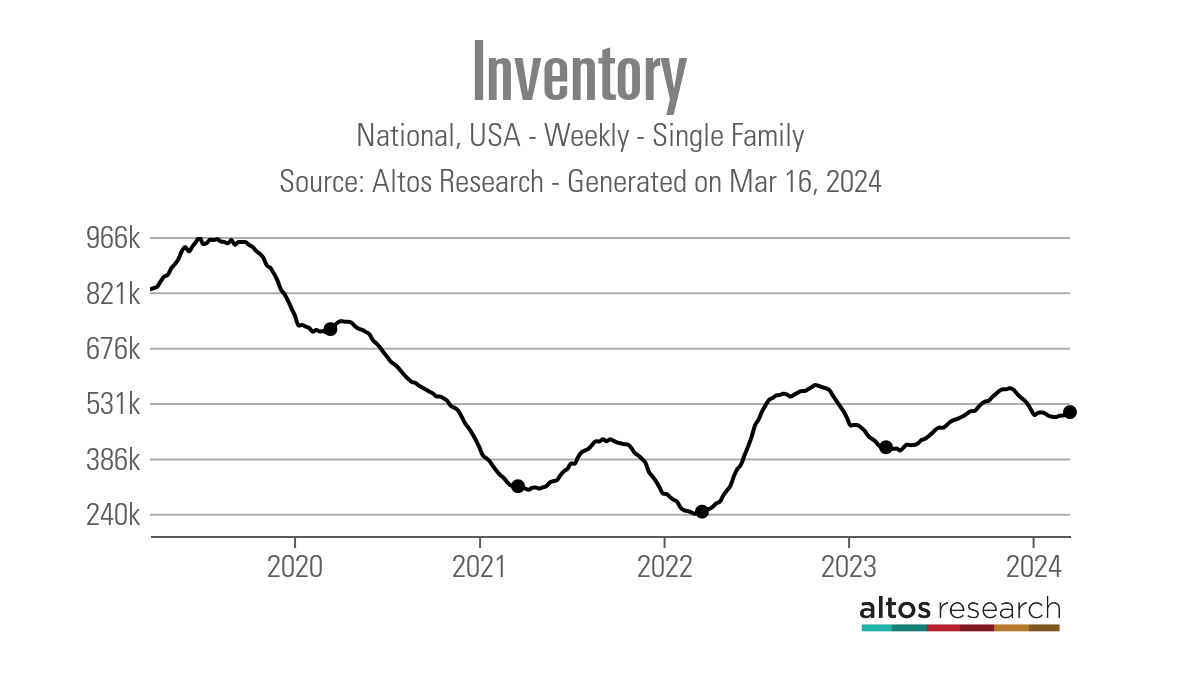

Weekly housing inventory data

One positive story for me in the housing industry this year is that inventory is increasing year over year, both in active inventory and new listing data. I know it’s not a big deal, but growth is growth. One benefit of rising interest rates is that inventory may increase in the post-2010 qualified mortgage world, as long as rising interest rates soften demand. Historically, there hasn’t been much growth, but growth is growth.

Last year, the seasonal inventory bottom occurred on April 14th, which was the longest period of time for a seasonal inventory bottom to be found. This means we will see above-normal inventory growth until after the 2024 tax day.

Last week’s inventory status looked like this.

- Weekly stock fluctuations (March 8th to 15th): Inventory has increased 500,579 to 507,160

- Same week of the previous year (March 9th to 16th): In stock 413,199 to 414,967

- The all-time low for inventory was in 2022. 240,194

- The peak of inventory in 2023 is 569,898

- For some background, here’s this week’s active list: 2015 was 982,639

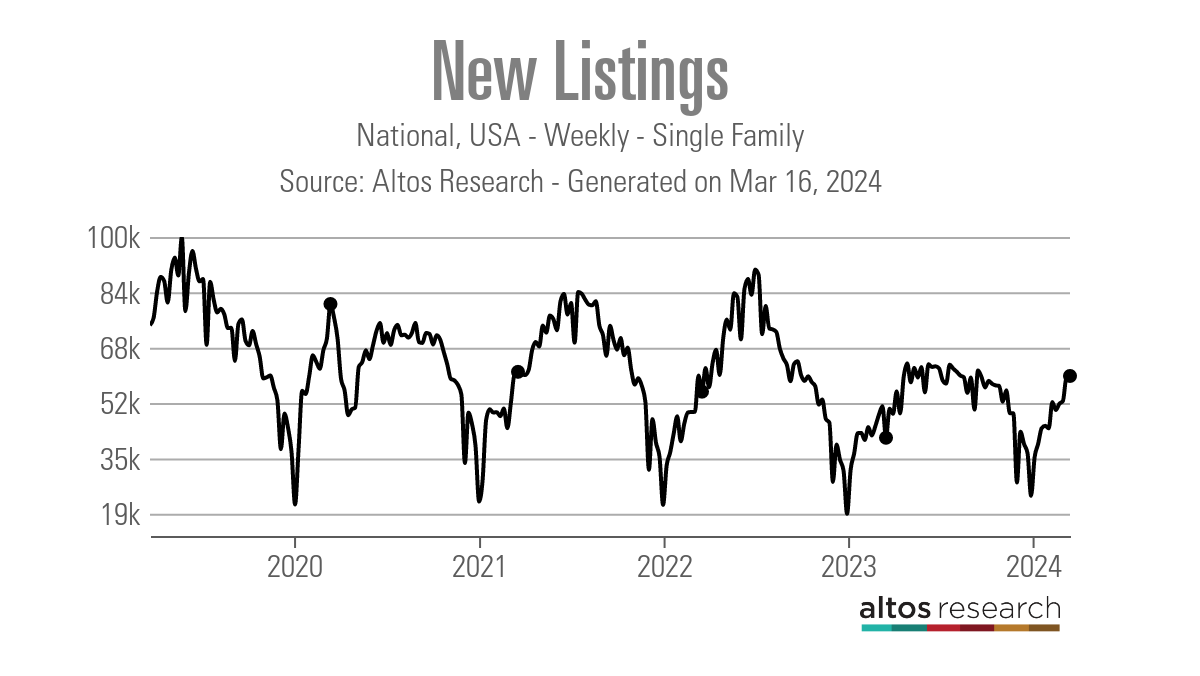

New listing data

The number of new properties is increasing year by year, which is also a positive factor for housing. Last year, II identified a trend where new listing data was forming a historic bottom, as rising interest rates did not necessarily cause the data line to fall. The growth was a little lighter than I expected. But as someone who didn’t support locking down mortgage rates on the premise that higher interest rates wouldn’t increase inventory, this year is a good test case.

Here’s weekly new listings data for the past few years:

- 2024: 59,542

- 2023: 41,415

- 2022: 54,542

For historical context, here is this week’s new listing data for 2010: 306,020.

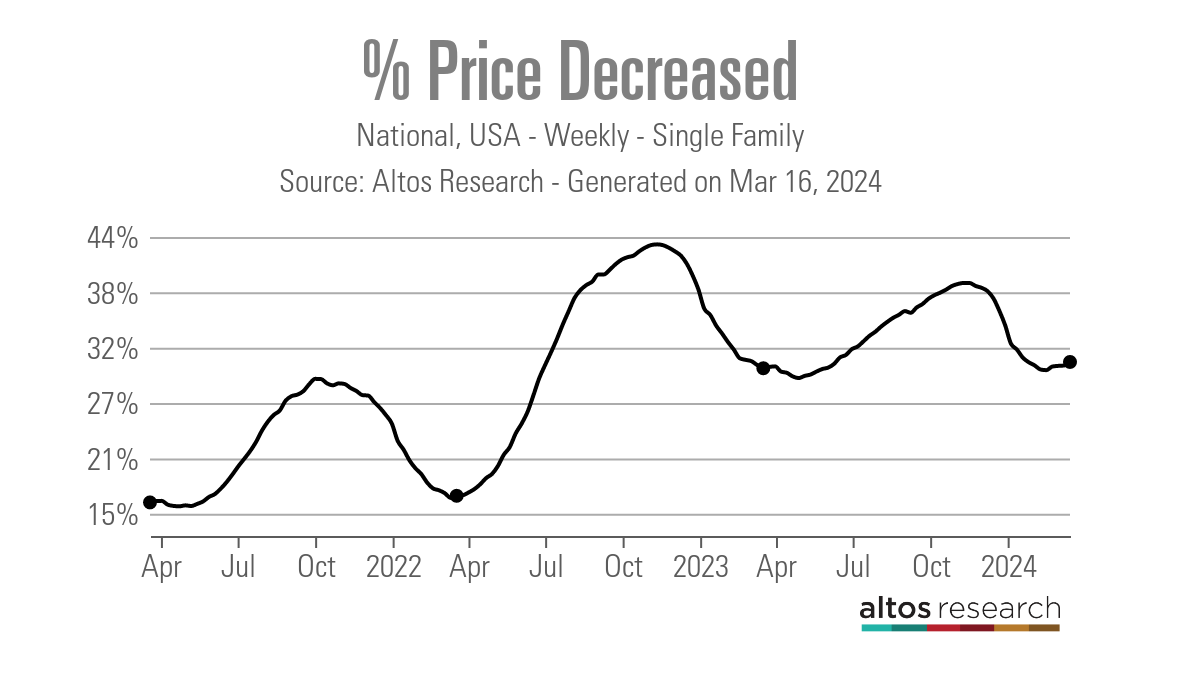

price reduction rate

Every year, one-third of all homes have their prices reduced before they go on sale. This is regular housing activity and this data line is highly seasonal. If mortgage rates rise and demand takes a hit, discounts could widen further. When interest rates fall, interest rates are lower than normal.

The number of homes eligible for price reductions should increase as the year progresses, as inventory is higher than last year and may have already found a bottom. The objective is to see how the mortgage rate variable affects this data line. So this week’s Fed meeting will be key to determining whether the 10-year Treasury yield rises further, which should lead to more bearish indicators.

Here’s the percentage of homes that reduced in price before selling last week and how that compares to the same week last year.

- 2024: 31%

- 2023: 30%

- 2022: 17%

One week ahead: Fed and housing data

Two things to watch this week are the Fed text and the dot plot. The dot plot should show that many Fed members plan to cut rates two or three times into 2024, with some members going in the opposite direction from that group. A ton of housing data will also be released this week, including builder confidence, housing starts, existing home sales, and Zillow home price data. But the key is FRB, FRB, and FRB!