(Bloomberg) The Federal Reserve’s frontline inflation gauge is trying to signal some easing from stubborn upward price pressures, underscoring the central bank’s caution about the timing of interest rate cuts.

Most read articles on Bloomberg

Economists expect the personal consumption expenditures price index excluding food and energy, due on Friday, to rise 0.2% in April, the smallest increase so far this year for the measure that gives a better snapshot of underlying inflation.

The overall PCE price index is expected to rise 0.3% for the third straight month, according to the median forecast in a Bloomberg survey. That increase this year contrasts with a relatively flat reading in the final three months of 2023, highlighting the Fed’s uneven progress in tackling inflation.

Fed Chairman Jerome Powell and his colleagues have stressed that they need more evidence that inflation is sustainably moving toward their 2% target before lowering the central bank’s policy rate, which has been at a 20-year high since July.

The PCE price index is expected to rise 2.7% year-over-year, while the core index is expected to rise 2.8%, both in line with the previous month’s levels.

Officials earlier this month agreed on their desire to keep interest rates higher for longer, with “many” questioning whether policy was tight enough to bring inflation down to target, according to minutes of their last meeting.

Read more: Officials rally around prolonged high interest rates, minutes show

The latest inflation numbers are accompanied by figures for personal consumption and income, which provide information on spending on services after demand grew robustly in the first quarter but retail sales were flat in April.

Bloomberg Economics:

“The report will offer encouraging signs that the deflationary process has not stopped completely. A cooling labor market has slowed income growth and consumers are gradually cooling off, which should provide continued deflationary stimulus for the rest of the year. However, inflation is likely to ease only very slowly this year as catch-up pressures on prices still persist.”

—Anna Wong, Stuart Paul, Eliza Winger and Estelle Ou, economists. For a more detailed analysis, click here.

Other data this week include a revised first-quarter gross domestic product report due out Thursday, with economists predicting growth will likely be slower than the government’s earlier forecast. The Federal Reserve will release its Beige Book on Wednesday, outlining the state of the nation’s economies.

Among the U.S. central bank governors speaking during the holiday-shortened week are John Williams, Lisa Cook, Neel Kashkari and Laurie Logan.

Looking north, Canada will release first-quarter gross domestic product data, with weaker monthly momentum in March and weak domestic demand likely prompting the central bank to eye a rate cut in June.

Other notable developments will include a possible rise in eurozone inflation, China’s industrial data and Purchasing Managers’ Index (PMI) readings, and Brazil’s price report.

Click here to read about last week’s events, and below for our outlook for the global economy.

Asia

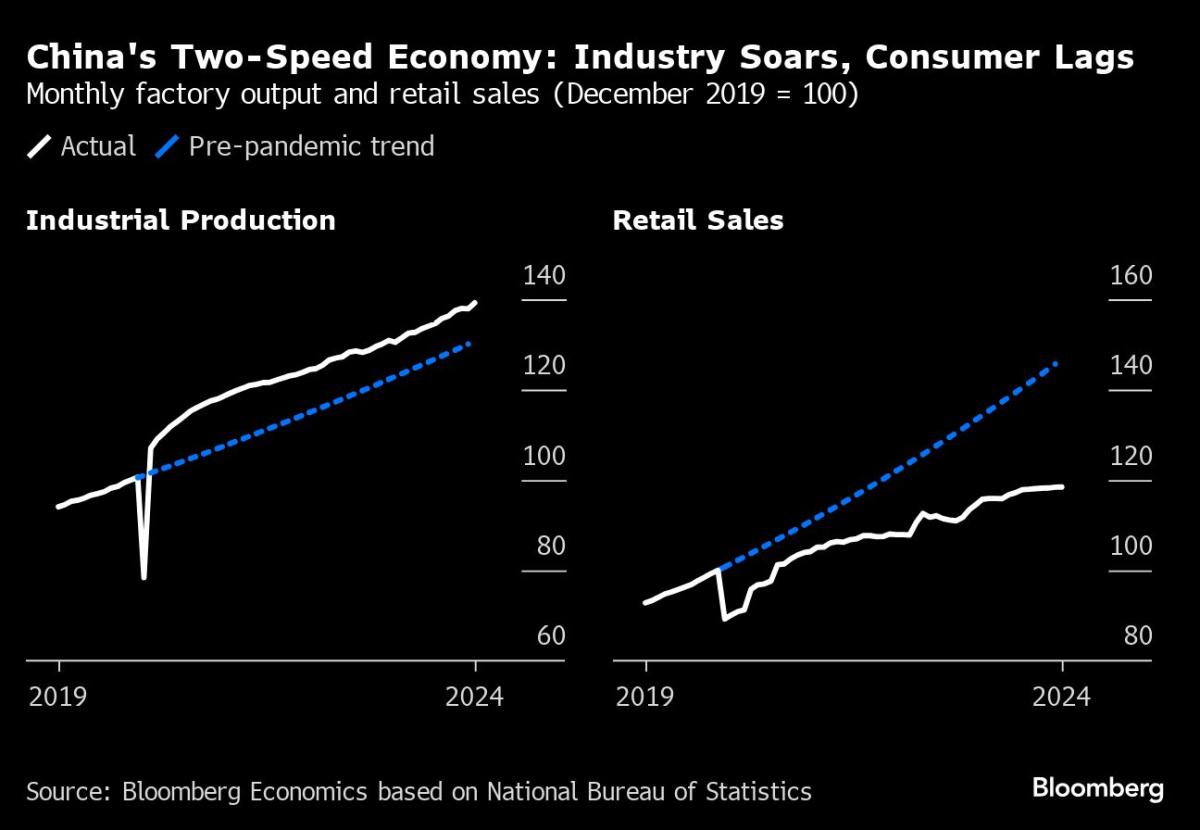

Attention will be on Chinese manufacturing next week, with industrial data due on Monday showing whether profits recovered in April after a sharp drop in March that saw profit growth in the first three months tumble to 4.3%.

Profitability is likely to remain under pressure due to persistent deflation in producer prices and weak domestic demand. China’s official manufacturing PMI data is due to be released on Friday, with a focus on whether it will remain above the 50 mark – the dividing line between recession and expansion – for a third consecutive month in May.

Also on Friday, Japan’s industrial production growth was forecast to slow, while retail sales were forecast to hold steady in April.

Tokyo’s consumer price index may rise slightly in May, portending an increase in the national figure.

Meanwhile, Japan and South Korea are pressuring Beijing by moving closer to the United States on a range of issues from security to semiconductor production, and China, Japan and South Korea will hold their first three-way summit since 2019.

Australian consumer price inflation is expected to slow to 3.3%, but remains too high for the Reserve Bank of Australia to keep interest rates unchanged.

Vietnam released CPI data this week, as well as industrial production, retail sales and trade.

At the central bank, Kazakhstan will set its benchmark interest rate on Friday.

Europe, Middle East, and Africa

Economists expect inflation in the euro zone will probably accelerate to 2.5% in May, after the underlying reading stopped declining for the first time since July and is expected to remain at 2.7%.

National data, starting with Germany on Wednesday and in line with euro zone-wide data, are expected to surprise three of the region’s four biggest economies, with inflation seen slowing only in Italy.

The results put the ECB at a disadvantage in reaching its 2 percent target, but one month’s worth of data is unlikely to derail its plans since officials have consistently signaled a quarter-point cut in interest rates on June 6. Still, some policymakers are arguing there should be no rush to ease further.

“It’s becoming increasingly likely that we’ll see the first rate cut within 13 days,” Bundesbank President Joachim Nagel, a policy hawk, said in an interview on Friday. “If there’s a cut in June, then I think we’ll have to wait, maybe until September.”

Other euro zone reports include Germany’s Ifo business confidence index on Monday, the ECB’s inflation expectations survey on Tuesday and an economic confidence index on Thursday.

ECB officials scheduled to speak next week include chief economist Philip Lane and the presidents of the Netherlands, France and Italy. A pre-decision blackout period begins on Thursday.

The Bank of England has already gone quiet, cancelling all speeches and public statements by its policymakers during the campaign period ahead of the UK general election on July 4th.

Elsewhere in Europe, attention is focused on the Swedish Riksbank’s financial stability report on Wednesday and a speech in Seoul by Swiss National Bank President Thomas Jordan.

Several monetary policy decisions are scheduled across the broader region.

-

The Bank of Israel is expected to keep interest rates steady at 4.5 percent on Monday to contain inflationary pressures largely due to the war and support the shekel. Governor Amir Yaron has eased monetary policy, wary of a further widening gap between Israeli and U.S. borrowing costs.

-

Ghana’s monetary authority is set to keep interest rates unchanged at 29% on Monday in an effort to tame persistent inflation and support the struggling currency.

-

Mozambican policymakers were poised to cut borrowing costs on Wednesday, with consumer price inflation expected to remain in single digits for the rest of the year.

-

And on Thursday, a day after elections that threaten to cost the ruling African National Congress its majority, South Africa’s monetary authority is expected to keep interest rates unchanged at 8.25%, even though inflation has yet to return to the midpoint of its target range of 4.5%.

latin america

Brazil will next week release mid-month figures for the country’s benchmark consumer price index as well as May’s reading of its broadest inflation gauge.

The combination of Brazil’s tight labor market and a weak currency has already kept inflation close to consensus expectations for the end of the year, likely limiting the room for further deinflation from current levels.

The IPCA-15 price index fell back below 4% last month after surging by more than 5% in September, just two months after hitting 3.19%, below the central bank’s 2023 target.

Also in Brazil, the central bank released its weekly survey of economists on Monday showing inflation and interest rate expectations rising again, as well as increases in the national unemployment rate, total loan outstanding and budget balance.

Chile released six indicators for April, with the key figures being unemployment rate, retail sales, industrial production and copper production.

Mexico’s schedule will be dominated by the release of the central bank’s quarterly inflation report, followed by a press conference hosted by Governor Victoria Rodriguez.

Earlier this month, BNP Paribas revised upwards its inflation forecast through the third quarter of 2025, while Wednesday’s report will reveal the bank’s revised GDP forecast.

Mexico’s labor market data for April is due to be released on Thursday, with early consensus calling for the unemployment rate to rise from a record low of 2.28% hit in March.

–With assistance from Robert Jameson, Piotr Skolimowski, Monique Vanek, and Laura Dhillon Kane.

(Updates in Asia Summit section)

Most read articles on Bloomberg Businessweek

©2024 Bloomberg LP