I first used the term ‘extremely unhealthy’ in March 2022, when inventories were at record lows and demand was strong. Both credit and inventory channels have changed since 2010 due to the Qualified Mortgage Law and his 2005 bankruptcy law reforms. This means homeowners with less financial stress should sell their homes before the unemployment recession. This kind of activity had been going on for several years before the 2008 job-loss recession.

Before COVID-19 hit us, homeowners were in very good shape, and after refinancing their most important debts to lower payments, they were even better. Also, their wages are rising faster during periods of inflation. I was concerned that the abnormally low level of housing inventory would continue for an extended period of time, leading to an unhealthy rise in house prices, and that is what happened between 2020 and 2023.

Big increases in house prices are not good, especially if they happen quickly. Rising mortgage rates in this environment could lead to a massive demand disruption, and that’s what is happening.

Pre-home sales are approaching 21st century lows, but even with that reality, the number of days on the market is still in the teens, as the chart below shows.

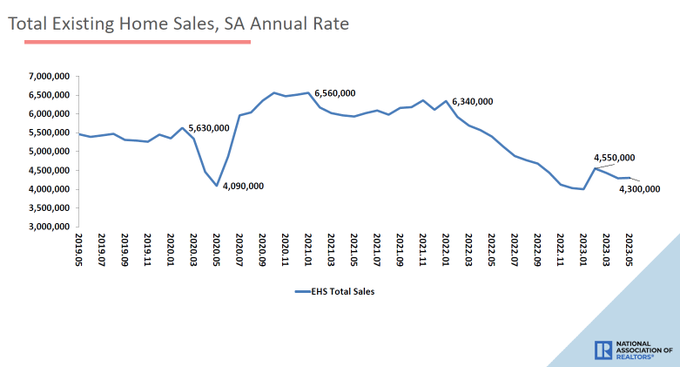

from NAR: total Second-hand home salesCompleted transactions – including single-family homes, townhomes, condominiums and co-ops – increased 0.2% from April to a seasonally adjusted annualized rate of 4.3 million in May. Year-on-year, sales declined by 20.4% (down from 5.4 million units in May 2022).

Home sales this month were stronger than expected, as they were trending downward month by month. We had a big sale three months ago and I think that’s going to be our peak sales this year. So far, the decision has been correct. Because I don’t think mortgage rates will go down enough to increase demand from this print.

NAR survey: Total existing home sales rose 0.2% from April to a seasonally adjusted annual rate of 4.3 million in May.

We want to play on the edge of the sales range for the rest of the year. The sales range must be within the following range: 4-4.6 millionthe same range I talked about after the huge sale print that took us. 4.55 million. Demand will undoubtedly weaken if the following trends 4 million But the trend above 4.6 million means the demand for mortgages is much higher.

I don’t see any data over 4.6 million over the term unless mortgage rates drop significantly from what they are now.There is a better case that can be reached by 4 million If mortgage rates stay high and new listings data begin to decline seasonally.

Well, from now on A grossly unhealthy part of the report.

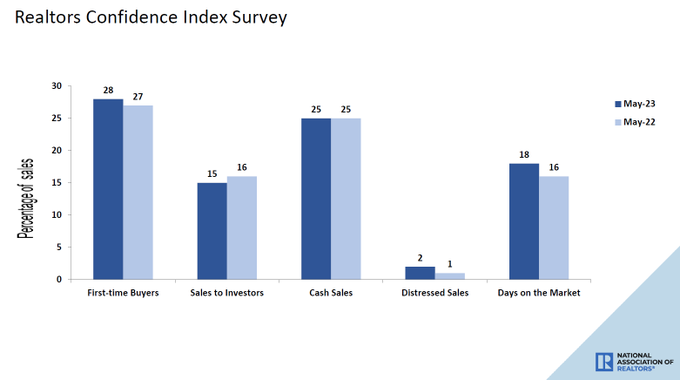

NAR survey: First-time buyers accounted for 28% of sales in May. Private investors bought 15% of the homes. All-cash sales accounted for his 25% of deals. Distressed sales accounted for his 2% of sales. Usually the property remained on the market for his 18 days.

The market has been close to 2022 levels for a few days, but this is not because demand is surging but because demand is stabilizing. As the year progresses into the second half of 2022, housing demand has deteriorated, with more than 30 days on the market, meaning the housing market is no longer terribly unhealthy.

However, as demand stabilized, the number of days on the market has decreased.

There’s not much you can do here, mortgage rates are close 7%, and people do not sell. So when demand stabilizes, the number of days on the market can be shorter. The percentage of cash buyers is the same year-over-year, and nearly everything in this survey isn’t far from his 2022 level.

From NAR: The total number of registered housing stocks at the end of May was 1.08 million, an increase of 3.8% from April, but a decrease of 6.1% from a year ago (1.15 million). At the current sales pace, there are 3.0 months of unsold inventory, up from 2.9 months in April 2022 and 2.6 months in May.

Yes, housing inventory is declining year by year. Inventory increased month by month, but this year’s spring inventory data showed a walking dead, so the growth was very poor, and in June, it was negative compared to the same month of the previous year. I can’t stress enough how bad it is. CNBC One month ago.

As you can see from the chart below, despite the biggest home sales crash in history in 2022, total inventory data is still far from the historically normal level of 2-2.5 million.

Total NAR ATP back in 1982:

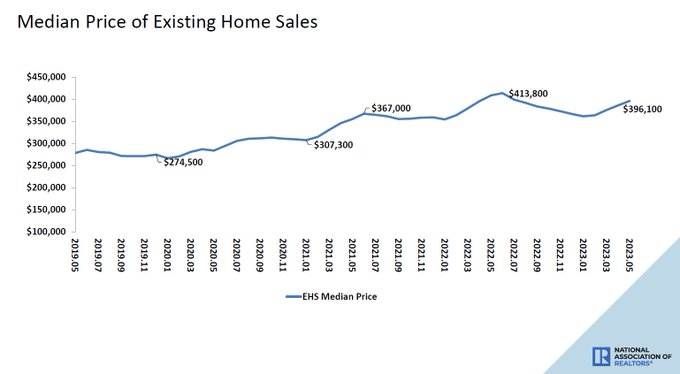

of Existing Home Sales Report I was a little surprised by the demand. But the point for me is that the days of market data have turned housing into a terribly unhealthy housing market. The median selling price data is down year-over-year, and I welcome that, but when the monthly data is solid with price increases, a lot of people put too much weight on the median selling price. I don’t.

Even if there are no big screams about the year-over-year price decline, it probably has something to do with the firmness of prices in all monthly price indices that are not tied to the median selling price.

NAR survey: The median resale home price for all home types in May was $396,100, down 3.1% from May 2022 ($408,600). Prices rose in the Northeast and Midwest, but fell in the South and West.

I publish a weekly housing market tracker that looks at the state of my inventory data, so I can see what’s happening in near real time long before my monthly sales report arrives. This is important because the dynamics in the housing market are changing. From a market where inventory increased and demand plummeted to a market with stable demand.

In contrast, inventory growth has been so slow this year that the NAR data is already negative year-over-year. We became aware of this change on November 9th, 2022, but now, in June of 2023, the data confirms what we were tracking at the time.

In this podcast, I explored the housing market recession as a whole last year, and it’s ironic that we’re back in a horribly unhealthy housing market.