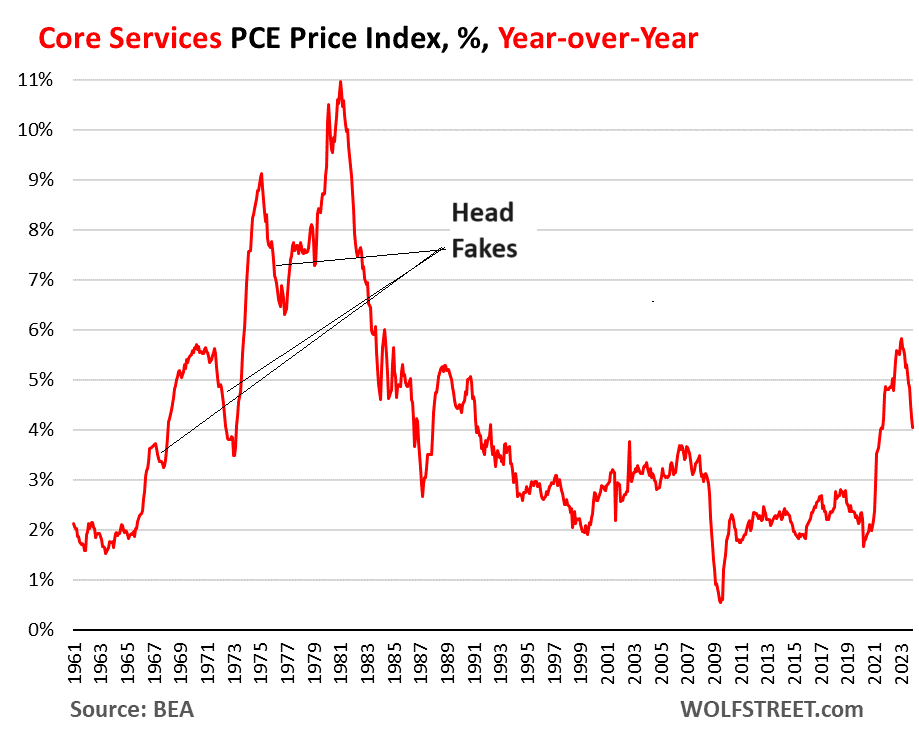

And look back at the head-scratching core service inflation that caused chaos last time with this kind of inflation.

Written by Wolf Richter of Wolf Street.

Let’s face it, the Fed keeps talking about this, but no one is listening: The “core services” PCE price index has been stuck at 3.5% annualized for the past six months, month-on-month. Housing inflation, which has accelerated to 4.0%, has remained at an annualized rate of approximately 6.7% over the past six months, and other core service components remain challenging.

According to today’s Bureau of Economic Analysis data, the PCE price index for core services rose 0.33% in December compared to November, the second consecutive acceleration. This corresponds to an annual increase of 4.0% (blue).

The 6-month moving average, which compensates for the large ups and downs in the monthly data, has accelerated to 3.5% and has been within this range since August, after decelerating sharply in early 2023 (red).

Core services are important because they are where consumers spend most of their money. That’s why Fed directors are almost unanimous in not rushing to cut interest rates, but are taking a wait-and-see approach with an eye on core services. It’s okay if it disappears.

However, on the surface, the PCE price index looks encouraging. This trend has continued in recent months, with the overall PCE price index increasing by 2.6% year-on-year in December, the lowest level since March 2021. Additionally, the Core PCE Price Index was +2.9% year-over-year, also the lowest level since March 2021 and on track for the Fed’s 2% target.

The factors that led to a year-on-year decline in these inflation measures remained the same in recent months. Energy prices are plummeting, durable goods prices are plummeting after huge increases in 2020 and 2021, and food inflation is cooling (prices are still very high). (high level but slowly), there is a good ‘base effect’ when compared to a year ago.

However, energy prices will not fall forever and will eventually resolve. Durable goods prices also won’t plummet forever, but they may fall for a while to provide some relief from the price spikes experienced in 2020 and 2021. And if the year-over-year basis is the lower inflation rate in 2023, the base effect will expire this year.

A similar scenario emerges for December’s CPI inflation index, which we have discussed in detail here with a number of graphs.

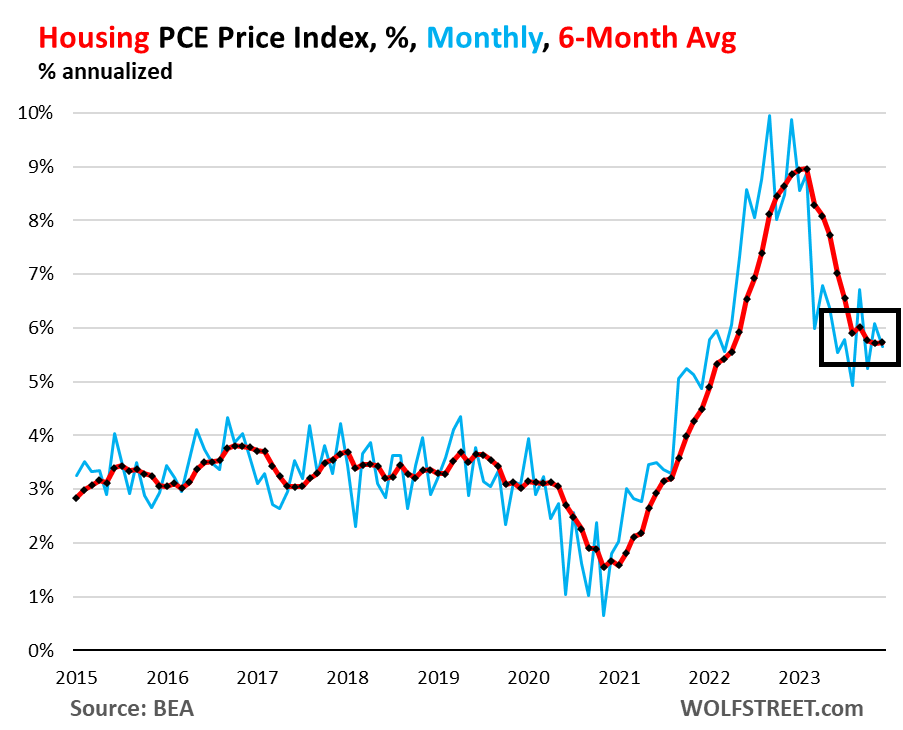

Housing inflation is still hot and won’t cool down. The PCE price index for housing in December increased by 0.46% from November, and after a sharp deceleration in early 2023, it has remained in this range since March. This corresponds to an annual interest rate of 5.7% (blue in the figure below).

The housing index is broad and includes rent factors for tenant-occupied housing. Imputed rent for owner-occupied housing, apartment housing, and rent for farm housing. This is the largest component of the core service.

The annual six-month moving average, which indicates recent trends, also rose by 5.7% in December and has remained in the same range since August (red).

In other words, the PCE price index for housing appears to be stuck at 5.7%. This stubborn inflation in housing is a blow to the theory that has been floated for 18 months that housing is behind and we know it will be a problem. The rise is not as steep as before, but it remains hot. And it became persistent.

The major categories of core services in the PCE Price Index are annualized as six-month averages of month-over-month changes:

| Core services, major categories, 6-month average, annualized | ||

| housing | 5.7% | Description and diagram above |

| Utilities other than energy | 2.5% | Water, sewer, garbage |

| health care | 2.5% | Doctors, outpatient clinics, hospitals, nursing care, dentistry, etc. |

| transportation service | 6.1% | Automobile repair/maintenance, automobile leasing/rental, public transportation, airline tickets, etc. |

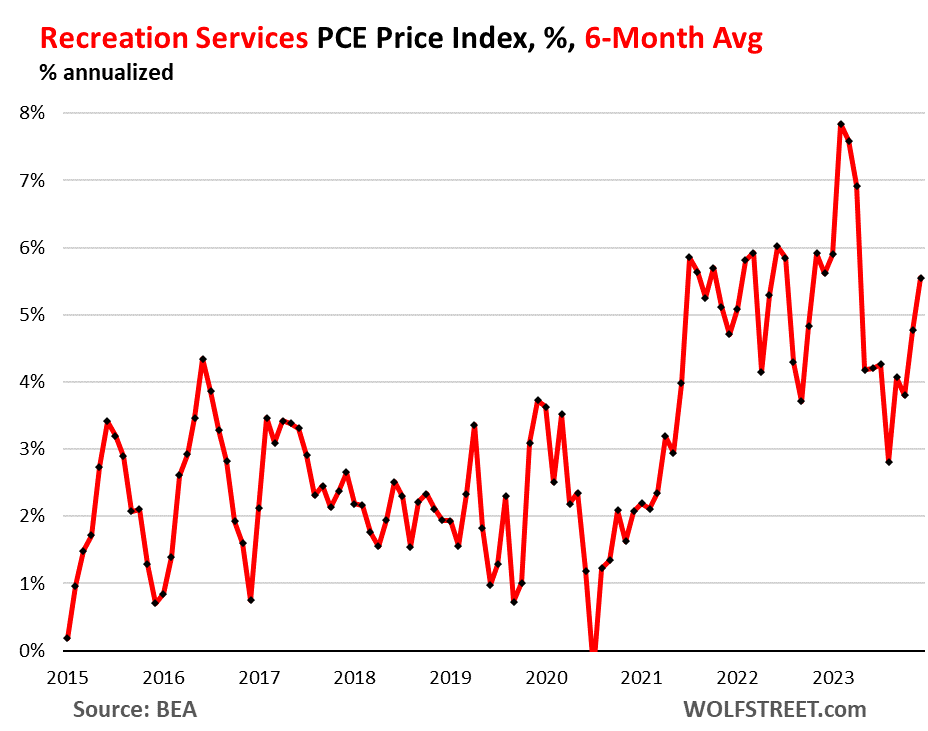

| recreational services | 5.6% | Concerts, sports, movies, gambling, streaming, veterinary services, package tours and more. |

| Food and beverage services, accommodation services | 2.8% | Food and drinks in restaurants, bars, schools, cafeterias, etc.Accommodations such as hotels, motels, and schools |

| Financial operations | 3.5% | Fees and charges for banks, brokers, funds, portfolio management, etc. |

| insurance | 2.8% | Various insurance including health insurance |

| Other services | 0.1% | Collection of other services |

Inflation in transportation and recreation services has accelerated based on six-month moving averages, with the PCE price index for transportation services increasing by 6.1% and the index for recreation services increasing by 5.6%.

![]()

Last time’s head fake.

Service inflation can prove difficult to beat and can lead to major fraud. The last time we had this kind of inflation spike was in the 1970s and 1980s, and many times we wondered if we were fooling ourselves with inflation, but in the end we were fooled by the inflation deception. I found out that In 1981 he was on his way to a peak of 11% and on core serve he had three head fakes.

Enjoy reading and supporting Wolf Street? You can donate. I appreciate it very much. Click on the beer and iced tea mugs to see how:

Would you like to receive email notifications when new articles are published on WOLFSTREET? Sign up here.

![]()