Has the recent rise in mortgage rates impacted new listings data more than usual? Hopefully not, but last week saw a notable drop in new listings. The Fed spoke at Jackson Hole last Friday, but mortgage rates didn’t move much. Purchase requisition data also dropped further each week.

- Weekly active listings increased slightly 6,618.

- home loan interest rate 7.37% to 7.48% and back 7.37%

- Purchased apps decreased 5% week-over-week.

weekly housing inventory

Let’s focus on the big drop in newly listed stocks. I hope this is temporary and has nothing to do with rising mortgage rates. While we were pleased with the steady decline in new listings over the past two months, we have seen a significant drop this week. With mortgage rates soaring to 23-year highs and new-property data dwindling, I thought there might be a corollary between the two. I don’t usually put a lot of weight on one-week data, but rates had just hit new highs, so I was mindful of this possibility. As you can see below, this data line was slowly and regularly decreasing over the course of the season, but picked up speed last week. Hopefully this will change course next week.

- July 21: 63,375 new listings

- July 28: 62,525

- Aug 4: 61,490

- August 11: 60,759

- Aug 18: 60,295

- August 25th: 55,291

The total number of active listings is up slightly from last week, but still too slow for my liking. However, here comes seasonality. We would like to extend the seasonality a bit more to ensure we have more active inventory in the system before winter.

Weekly inventory fluctuation (August 18th to August 25th): Inventory increased from 496,541 to 503,159

- Same week of the previous year (August 19th to August 26th): Inventory 551,458 to 554,748

- 2022 inventory bottom is 240,194

- So far, stock peaks for 2023 are: 503,159

- For context, see this week’s active list. 2015 was 1,216,061

As you can see from the chart below, inventories have been negative year-over-year since June. Compared to the slow zombie movement of 2023, last year’s occupancy inventory rocketed.

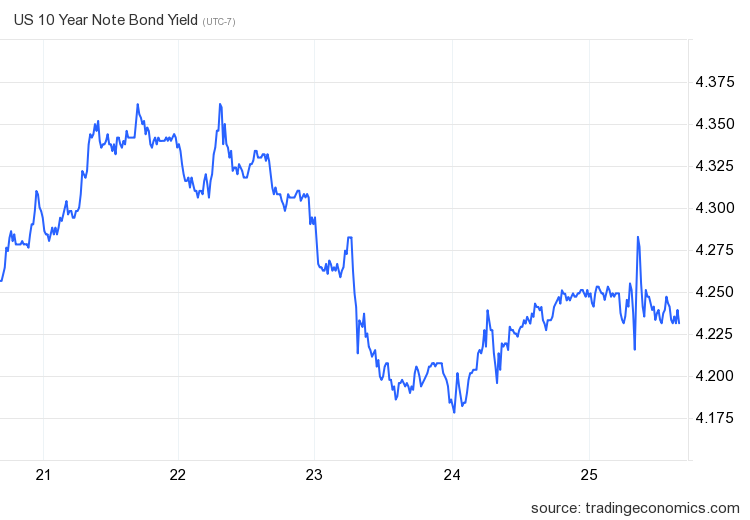

Mortgage Rates and Bond Yields

This week has been an important week for 10-year bond yields and mortgage rates.We talked about how important it is for us not to close above 4.34% After that, the bond market will sell even more.This could lead to higher mortgage rates 8%. However, it held the line last week and closed below the peak. 4.25%fExpected levels of 10-year bond yields.

For this week and the rest of the year, my focus is solely on whether the 10-year yield can finish above this level. 4.34%. The farther away from that level, the better. Lower inflation growth hasn’t helped mortgage rates this year as the economy is still holding up, as you can see from the chart below.

Purchase application data

Purchase requisition data decreased by 5% weekly, with year-to-date counts of: 14 positive and 17 minus print and a flat week. Starting from November 9, 2022, 21 positive print vs 17 minus print and one flat week. While home sales haven’t collapsed as they did last year, the lack of data for growth above 7% has made data on the future outlook for housing increasingly weak. Historically, we’re at extremely low levels, so it won’t take long to move the needle forward, but we’ll have to see interest rates fall.

Next Week: Jobs Week, Inflation Data, Pending Home Sales, Home Prices

It’s Jobs Week again this year, so look for job openings, ADP, unemployment claims, and Friday’s top four reports. Bureau of Labor Statistics job report. The key for the Fed is that it wants job growth to slow, wage growth to slow, job openings to fall, and unemployment claims to rise. Nationwide house price data is also updated.

Don’t miss the housing bubble burst debate on August 31st. Please register here.

The Fed’s flagship inflation report, the Personal Consumption Expenditure Report, is out this week. Here they want to see progress towards 2%. There are also pending home sales, and home sales have slowed, as purchase requisition data has shown for weeks. Buckle up everyone. Economic indicators are going to be a mess.