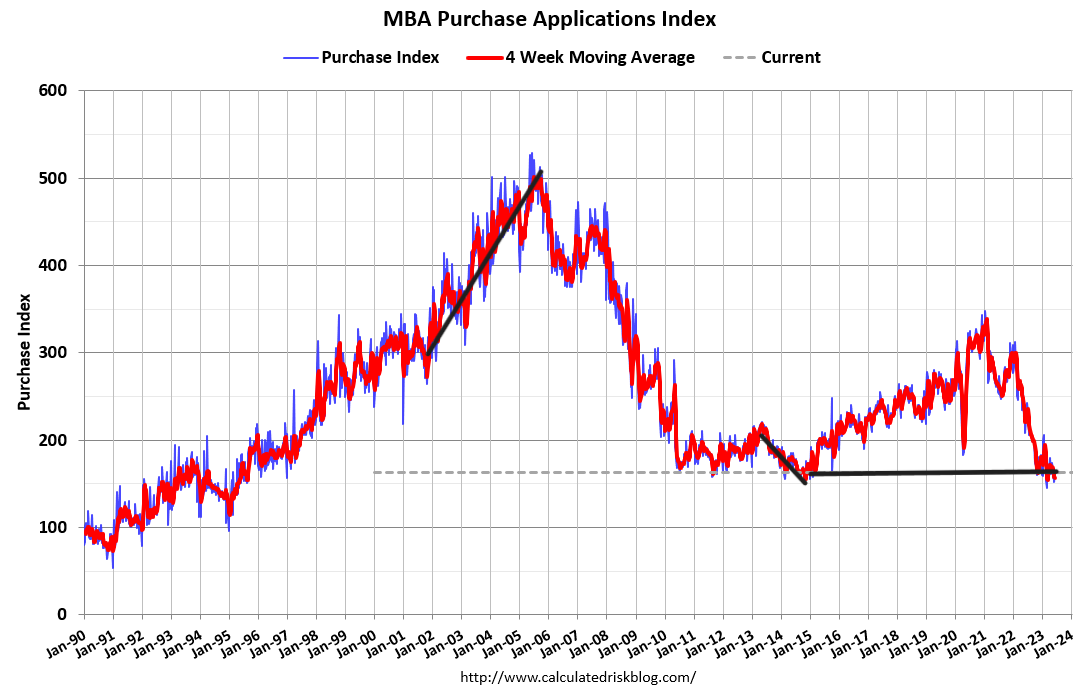

Mortgage rates were near 7% last week, but purchase offers were still able to pull off an 8% week-on-week gain. This was surprisingly powerful, but as I always stress, context is important. Purchasing Apps is breaking his four-week losing streak, and while the week-to-week decline has slowed, he is still in a four-week slump. Recent growth has broken that streak, but demand remains low.

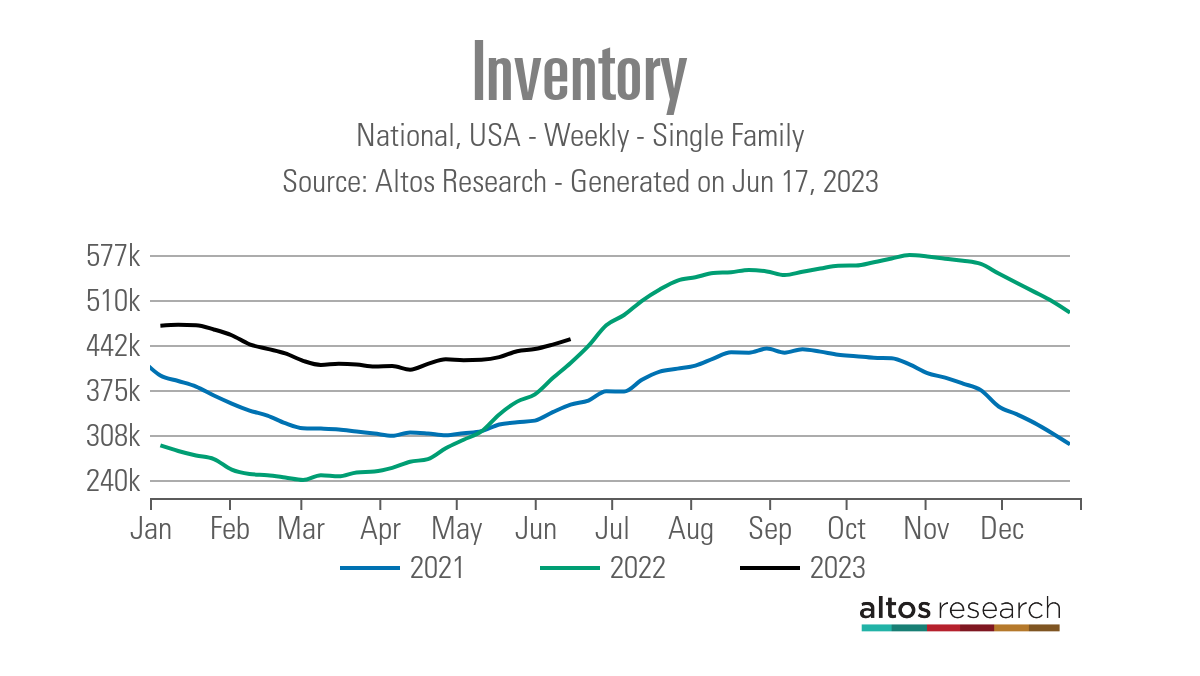

Active housing inventory increased, but new property data decreased. Mortgage rates were little changed last week. federal reserveannounced a moratorium on rate hikes and CPI inflation reporting.

Here’s a quick recap of last week:

- Increased available inventory 8,041 every week. Expect a couple of weeks with an increase of 11,000-16,000 units in stock.

- Mortgage rates remained within a narrow range of 6.94%-6.98%

- Purchase requisition data showed an 8% increase week over week

Purchase application data

Weekly growth last week was 8% and interest rates were near 7%, which was stronger than expected. However, last year saw the largest single-year waterfall crash in purchase application data, and since November 9, 2022, the data has continued to form a bottom zone.

This dynamic has transformed the housing market from a crash in home sales to what is now a stable market.I will explain how this happened this recent podcast. As you can see in the chart below, the collapse in requisition data has stalled and if this hadn’t happened, the housing market today would be discussed differently.

November 9th is a pivotal day for the housing market to turn. Since that date, the purchase requisition data, after adjusting for holidays, contains 18 positive prints and 11 negative prints. From the beginning of the year until now, I have made 11 positive prints and 11 negative prints.

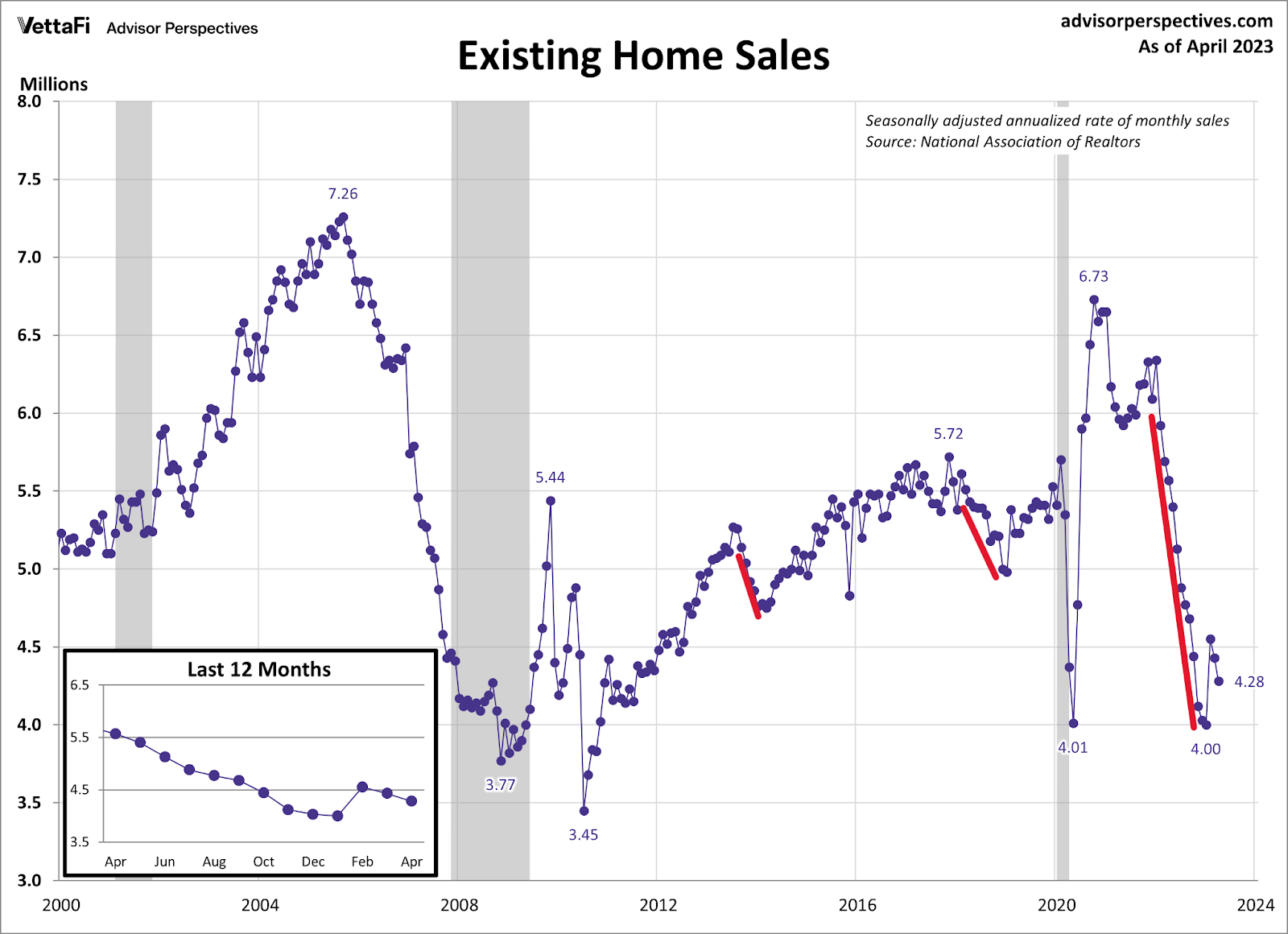

The growth seen between November 9th and February lasted long enough to provide the only major existing home sales performance of the year. In fact, there hasn’t been much movement since then, and this year’s sales should remain at 4-4.6 million units. However, if purchasing apps weaken further, this data line could fall below his 4 million.

Pre-owned home sales are on the horizon, but we don’t expect any big surprises in this week’s report. It cannot exceed 4.6 million this year without a series of positive purchase requisition data that would necessitate lower mortgage rates. Last year, when mortgage rates fell from 7.37% to 5.99% in just a few months, there was a flurry of positive purchase offer data fueling mass home sales. Imagine what would happen to the housing market if interest rates stayed between 5.5% and 6% for a year.

weekly housing inventory

This year’s home inventory theme is The Walking Dead musical chorus of zombies trying to escape their graves. Slowly and steadily slow! It took the longest time in U.S. history to find a bottom for seasonal inventories on April 14, and has been on a modest rally since then.

But it’s still on the rise! In the normal housing market, inventory always rises in the spring and then declines in the fall and winter. We wanted to stock more this year, but we will do what we can.

- Weekly inventory fluctuation (June 9-16): In stock 443,006 To 451,047

- Same week of the previous year (June 10-17): In stock 392,792 To 415,582

- 2022 stock bottom price 240,194

- So far, the peak in 2023 is 472,680

- For context, see this week’s active list. 2015 it was 1,173,793

As you can see from the chart below, inventory growth is so slow that the inventory data is on the verge of negative year-over-year growth. This happens when purchase requisition data is flat year-to-date. Of course, if demand weakens to some extent, the number of days on the market will increase and inventories can pile up.

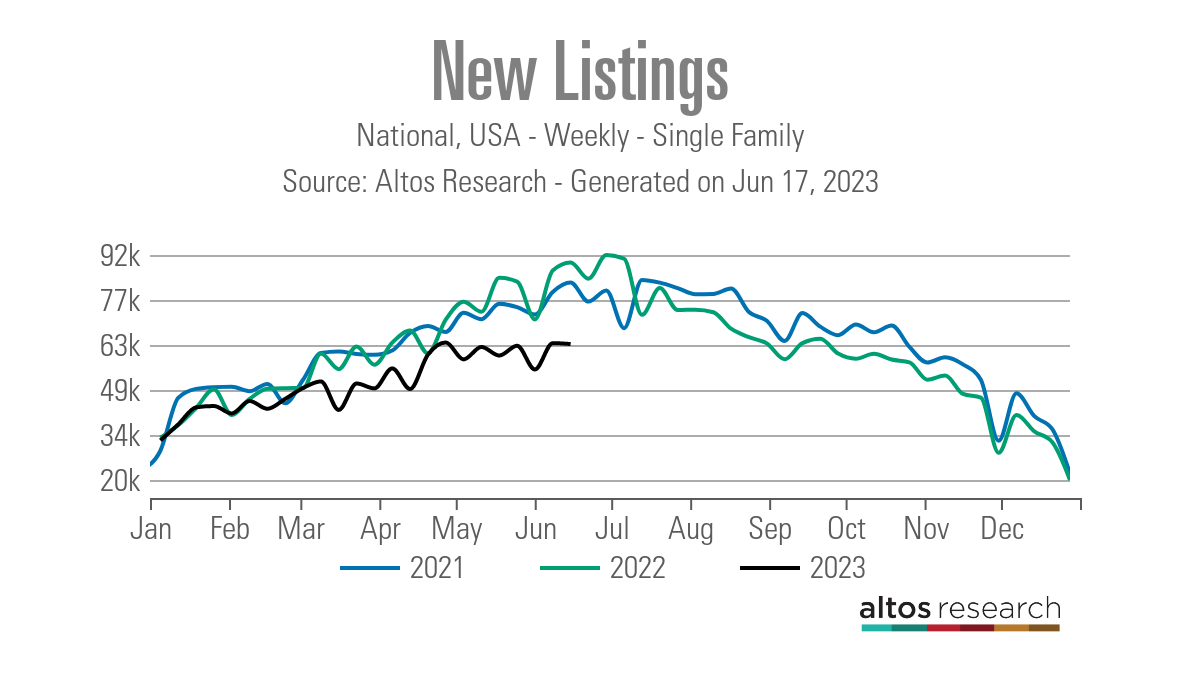

Another big topic in housing inventory is new property data. Since the second half of 2022, it has remained at a record low level. This trend continues throughout the year, so we are limiting the number of newly built houses that are eligible.

Below are some numbers to compare new listing data in recent years. As you can see, last year saw some growth year-over-year, but not this year.

- 2023: 63,293

- 2022: 89,166

- 2021: 82,815

There are only a few weeks left before the traditional IPO data dwindles, and only a few months left before the supply of traditional active listings dwindles. This week, NAR Existing Home Sales report updates inventory data line, but total inventory levels are still historically low

NAR Total Inventory Level:

- Here’s what we have in stock so far: 2-2.5 million

- 2007 was a little past its peak 4 million

- at present 1.04 million

10-Year Yield and Mortgage Interest Rates

It’s been a surprisingly boring week on mortgage rates, given the CPI report and Fed meeting. There was little change last week as mortgage rates remained in a very tight range. 6.94%-6.98%.

However, there has been an exciting move in the bond market that must be explained. First, the bond market reacted poorly to the CPI report. I wrote about the report itself here, but it still shows a downward trend in inflation.

However, as noted in a previous Weekly Tracker article, we debt ceiling measures, moved the market last week. Markets didn’t react well to the Fed meeting on what I said in this podcast. With all these events happening over the past week, the chart below shows how the 10-Year Treasury yield has moved.

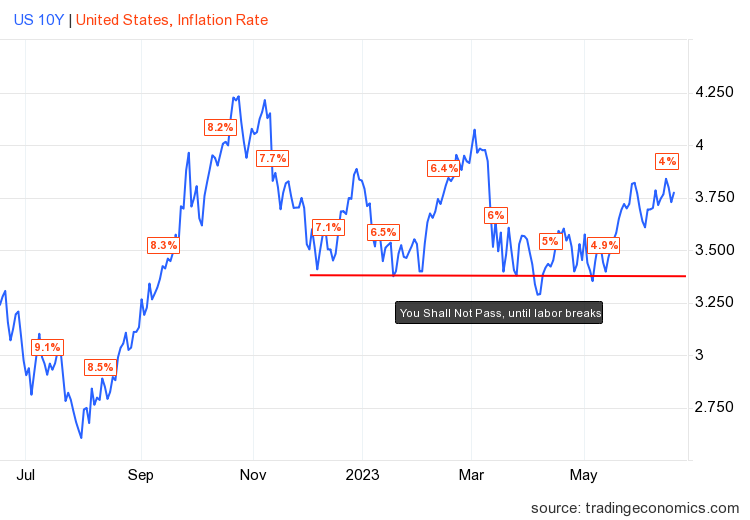

In my 2023 forecast, I wrote that if the economy held strong, the range of 10-year bond yields would be: 3.21% and 4.25%be equivalent to mortgage interest rates between 5.75% and 7.25%. As long as unemployment claims stay below his 323,000 four-week moving average, the labor market is doing well, which means the economy is doing well. .

I also note that the level over the last decade is 3.37% and 3.42% Breaking lower than that will be difficult. I call it Gandalf’s lines in the sand. “you shall not pass. “ Yes, it may be cliche, but I believe this level will be hard to break, and Gandalf had the right line for this bond market call.

So far in 2023, that line has held, as the red line in the chart below shows.Mortgage interest rates are in the range 5.99%-7.14%. However, the mortgage market has some problems.

ever since banking crisis Since its inception, the spread between 10-year and 30-year fixed mortgage rates has deteriorated, and mortgage rates have remained higher than normal. As you can see below, spreads changed notably when the banking crisis drama began and have not returned to their pre-drama trends. If this data line returns to normal, it would be a big win for the housing market. But until then, this was bad for the US economy.

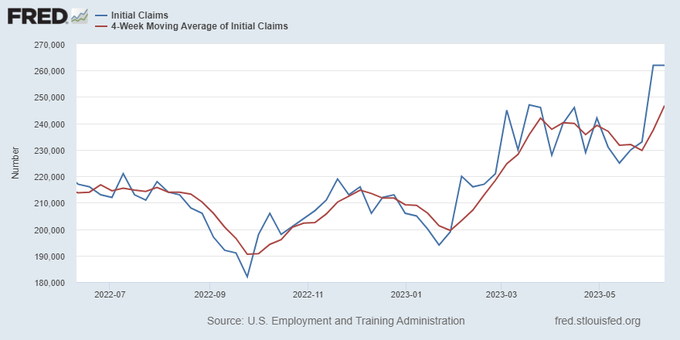

Another aspect of my 2023 forecast is that if unemployment claims exceed 323,000 The 4-week moving average could fall below the 10-year yield. 3.21% and go ahead 2.73%. There wasn’t much movement here last week. However, as you can see below, the labor market, while still very healthy, is not as tight as it once was.

from St. Louis Fed: The number of claims for unemployment benefits in the week ending June 10 was little changed at 262,000. 4-week moving average increased to 246,750

A week ahead: More housing data coming!

A series of housing data are released this week, including builder confidence, housing starts and existing home sales reports. Fed Chairman Jerome Powell is also scheduled to testify before Congress this week, which could lead to fireworks. Of course, I always keep an eye on unemployment claims data to see if I can find any further cracks in the labor market.

As for housing starts, we would like to see more apartments completed. Because the best way to deal with inflation is always to increase supply. There are also more 5 units under construction soon. This is very important. Because if rent inflation doesn’t happen again, that’s very important. Inflation like the 1970s will never be repeated.

So let’s hope for better home completion data this week. The best news for mortgage rates is lower inflation, and the best way to deal with this is to increase supply.