Here’s a quick recap of last week:

- Mortgage rates fell last week as 10-year yields fell for the first time since last year’s big rise in rates.

- Available stock is 823 Data for single-family homes and new listings are trending to all-time lows.

- Purchase request lost Four% Breaks 4th consecutive week of positive growth, still trending downward -35% Year after year.

10-Year Yield and Mortgage Interest Rates

The epic battle for 10-year yields last week saw it drop to significant levels. 3.42%-3.37% — The Gandalf Line in the sand. Bond yields have returned to their critical line after Friday’s jobs report, but I don’t put too much weight on holiday trading days. As you can see in the chart below, cutting that red line down was difficult, but it finally happened. This week’s trading in the bond market is exciting with upcoming inflation data.

For 2023, my projection for 10-year yields is a range of 3.21% and 4.25%,be equivalent to 5.75% To 7.25% mortgage interest rate. If the economy weakens and unemployment claims rise significantly, 10-year yields 2.73%, translation to 5.25% mortgage interest rate.

This assumes that the mortgage-backed securities market remains highly stressed, so the spread between 10-year and 30-year yields remains wide.

The banking crisis has put the entire year into a new floating spin as short-term rates predict rate cuts sooner than the Fed would like. Applications have increased recently, but have not reached my critical level, so all is well. 323,000 The 4-week moving average is still down. If short- and long-term rates continue to fall as economic data weakens, the Fed will be forced to cut rates sooner than originally planned.

The 4-week moving average is 237,500 as shown in the chart below.

Last Friday I wrote about the employment report and how it should now be revealed to everyone. federal reserve, the entrenched inflationary scare of the 1970s was just a joke. In the hottest labor market in history, wage growth has been declining year-on-year and has not gotten out of control.

Mortgage interest rates rise last week 6.44% dropped to the low of 6.16%the end time of the week 6.34%So despite all the drama this year, the 10-year yield has remained in range even with the nationwide banking crisis. We now have enough data to confirm that the labor market is not as tight as it appears. With his CPI inflation data and retail sales figures for this week, we could see another week of price volatility, depending on the data.

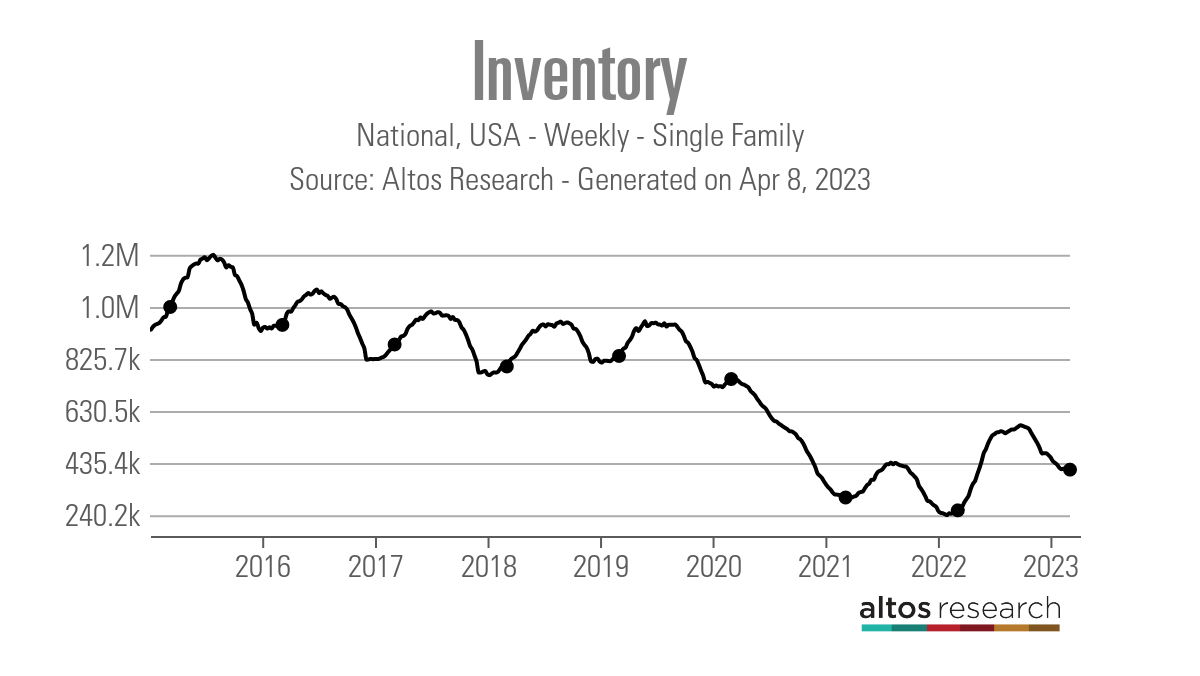

weekly housing inventory

Look at the Altos Research The big question with last week’s data is, did we see a seasonal bottom for inventories? Home inventories rose modestly last week, but we expect April to be a month of seasonal inventory increases.

- Weekly stock change (March 31st – April 7th): In stock 410,028 To 410,851

- Same week last year (April 1-April 8): Up 252,820 To 258,264

- The bottom of 2022 is 240,194

As you can see in the chart below, we are far from normal inventory channels and it is difficult to bring inventory back to pre-COVID-19 levels.

During the last expansion, mortgage rates ranged from 3.25% to 5% and inventories continued to slowly decline. Last year saw the biggest mortgage rate spike in history, which boosted inventories, but failed to return to 2019 levels.

Last year, the bottom of the weekly seasonal inventory was set March 4th. We need to see the bottom of the week in 2023. This year is similar to his 2021 data. April 9So April may be a turning point.

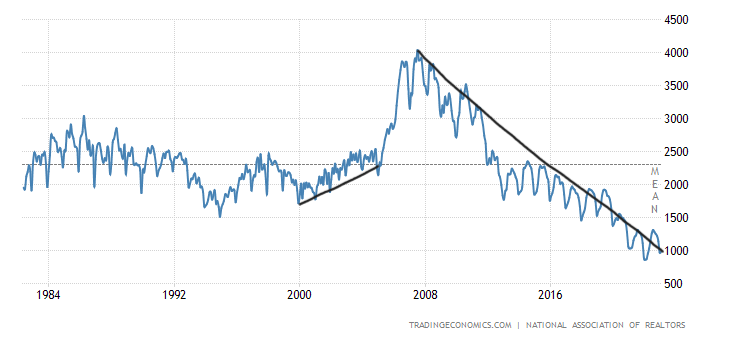

of NAR data Going back decades, we can see how difficult it was to get things back to normal on the active listings side. When sales plummeted in 2007, the total number of active listings was Four a millionWhile sales were currently at 2007 levels, 980,000 Total active listings per last existing home sale. Current housing inventory is not yet suitable for a healthy housing market.

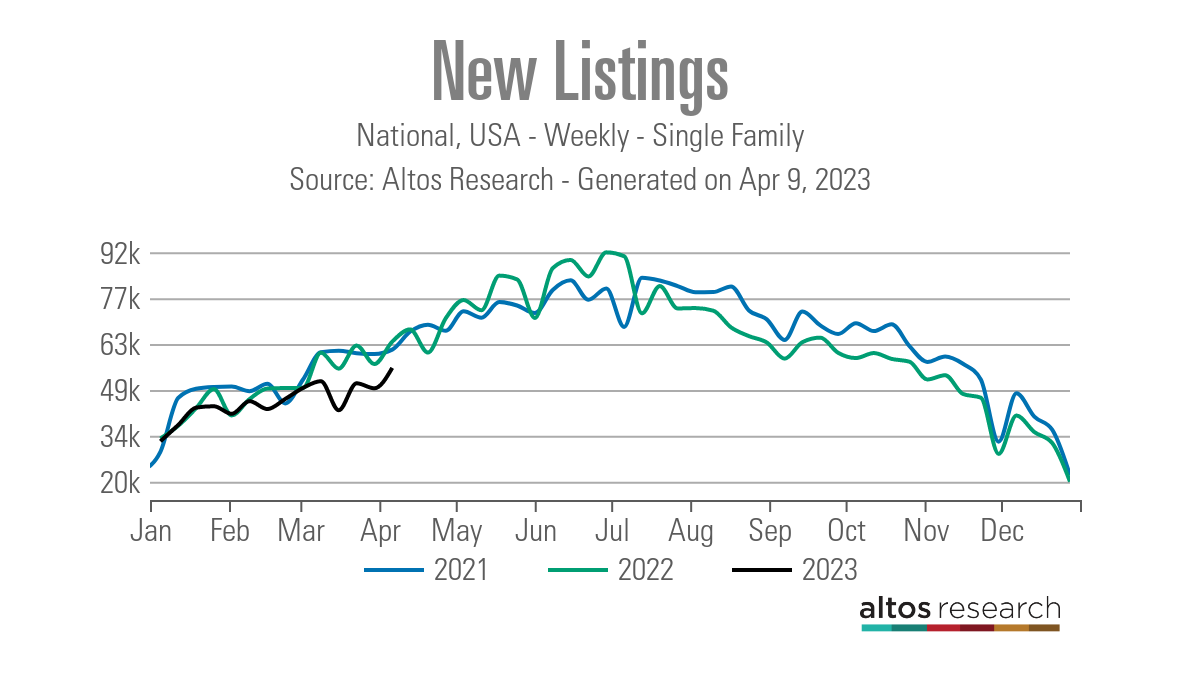

New listings data rose last week, but are still trending to record lows in 2023. But the fact that it’s returning to seasonal growth trends is a good sign. The last thing the housing market needs is a drop in new listing data, so the growth we saw last week is positive.

Here are the weekly numbers to see the difference in new listings over the past few years for the same week. Notably, the new listing data for 2022 was higher than his 2021. Not this year, of course, but if there’s one data line we’d like to see 2022 level above, it’s new listing data.

- 2021: 61,263

- 2022: 63,746

- 2023: 55,591

Compare new listings data each week with the previous year.

- 2015: 86,847

- 2016: 85,296

- 2017: 85,765

As you can see from the data above, homeowners are in no rush to sell as unemployment is still historically low and solid. US households are employed and live comfortably with low total housing costs, but the last thing on their mind is to give up that comfort for the unknown.

There are natural sellers in the US every year, but now US homeowners are sitting fairly at low fixed debt costs. As you can see below, year-on-year wage growth has slowed, but is still above what has been seen in the last decade.

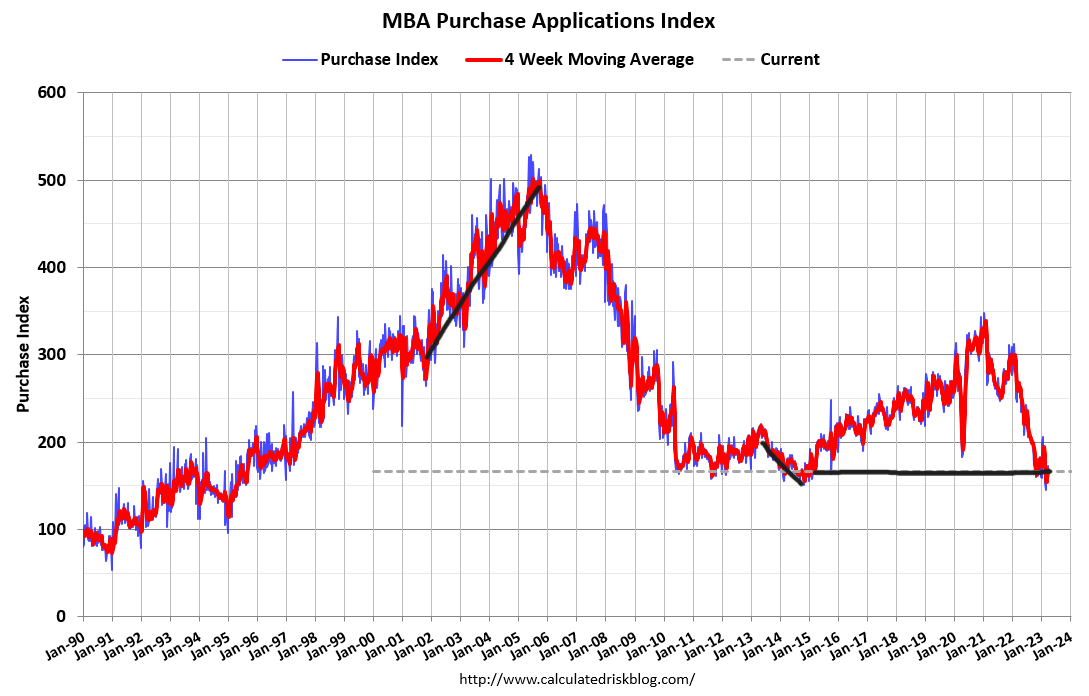

Purchasing application data

Purchase requisition data is one of the most improved housing market data lines since November 9, 2022. Pending home sales reports are also up for the third time in a row.

Purchase requisition data was down 4% weekly in the last report, breaking a four-week positive streak. The index is down -35% year-on-year. This is a reminder that year-over-year comps can be easy, especially in the second half. It will be interesting to see if lower mortgage rates move the data significantly in the next report.

As mortgage rates go up and down, the reporting of purchase requisition data becomes wild. Traditionally, this data line has not had this volatility, but 2022 was a historic plunge.home loan interest rate 5.99% To 7.10%with three negative prints, and this index reached the level last seen in 1995.

But as mortgage rates have since fallen by almost 1%, 7.10% Level found 4 of the last 5 prints to be positive. Looking at the key seasonal data lines for 2023, there are 7 positive prints and 5 negative prints.

Keep in mind that this line of data takes 30-90 days to reach sales data. Also, the seasonality of this data line is nearly complete. We generally place more weight on this line of data from the second week of January through the first week of May.

one week before Inflation and Mortgage Rates

Inflation week with two inflation reports. the most important thing Consumer Price Index Report, which indicates that the year-on-year low trend in inflation data will continue this week. In September last year, when the CPI report was released, CNBC asked me to talk about inflation My view was that 2023 would be a positive story as rent inflation slows.

This is important. Because it’s hard to keep inflation high unless rent inflation spikes. It’s a good thing for mortgage rates when rent inflation falls, because when inflation falls, growth falls. This is happening this year. Year-on-year inflation has fallen and will drop further in the next report. Learn more about why mortgage rates aren’t high.

Of course, it’s well known that the CPI report’s sheltered inflation rate lags far behind, so this week’s numbers are still unrealistic.

We also have a producer price index inflation report this week and retail sales on Friday. Retail sales are going to be interesting now. Because some of the credit growth we’ve seen so far (which keeps the economy expanding) is cooling off a bit.

And, of course, all eyes are on the bond market.as me recently talked about According to CNBC, the US housing market revolves around 10-year yields and what drives them up and down. We look at how economic data affects bond markets and mortgage rates. Every report becomes more and more important as Gandalf’s lines are broken and the labor market is beginning to soften somewhat.