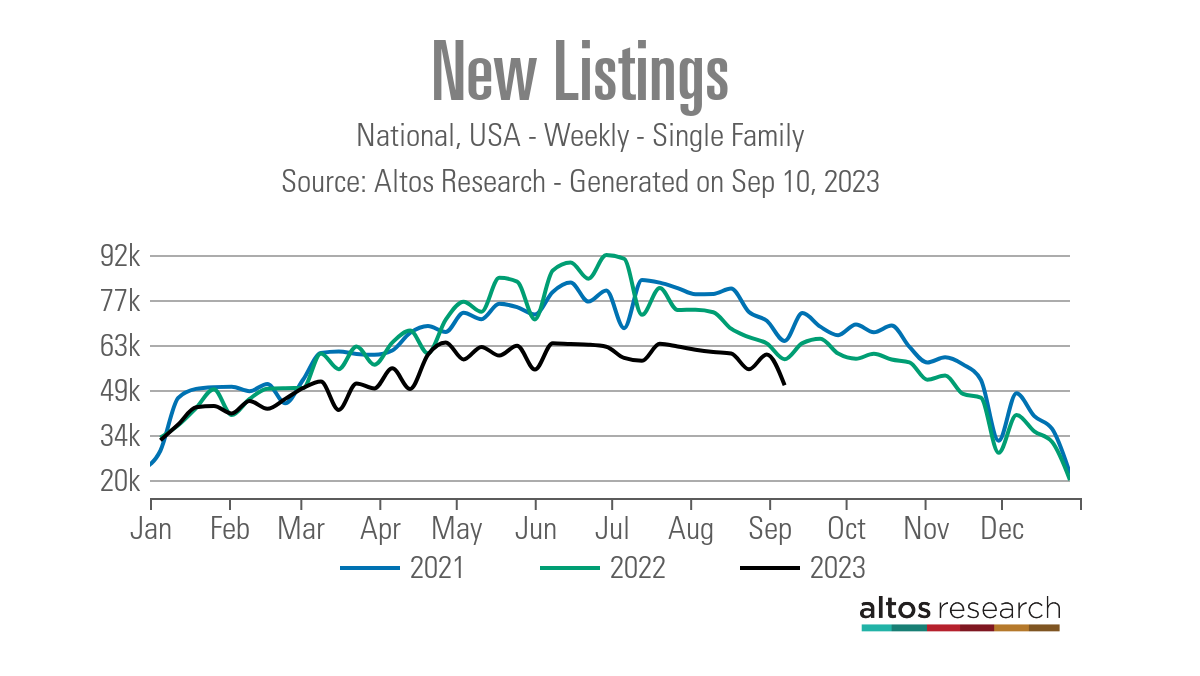

Last week, the number of new listings decreased significantly, and effective inventory was barely positive. Does this mean housing inventory is starting to decline seasonally? Here are the weekly numbers:

- Weekly active listings increased slightly 343

- Mortgage interest rates rose from 7.08% end the week with 7.22%

- Purchasing app has gone down 2% weekly

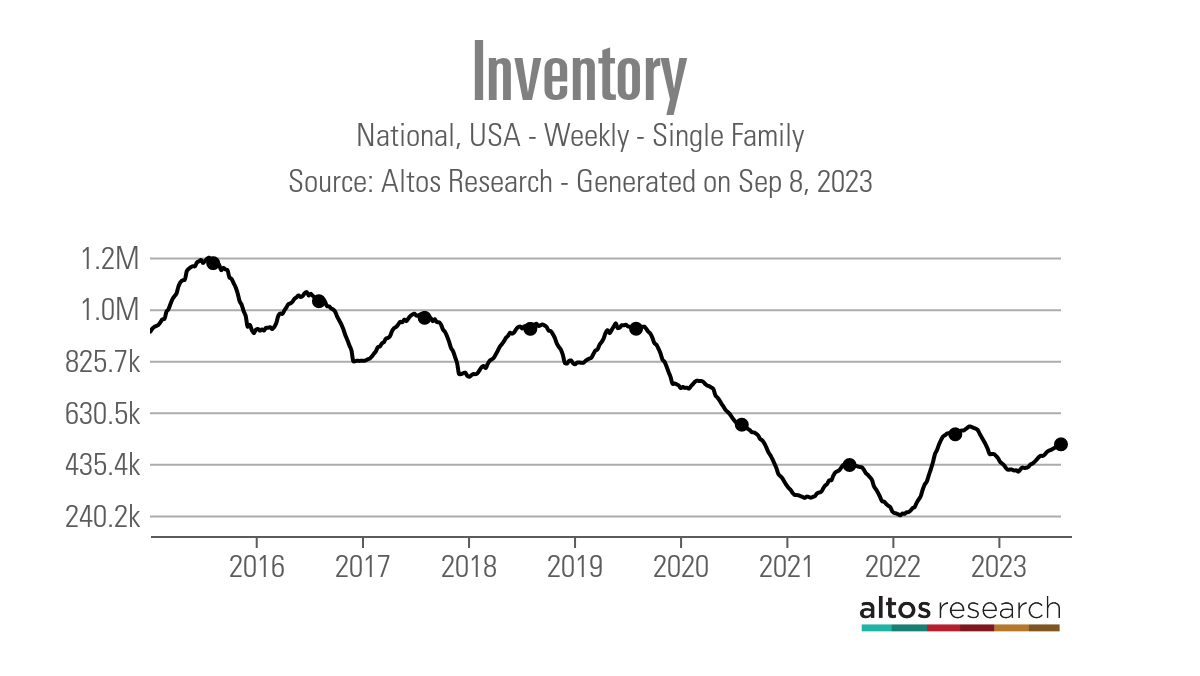

weekly housing inventory

At first glance, it appears that we are currently experiencing a seasonal decline in active inventory, as new listing data has decreased significantly and active listings have slowed to the point where active listing growth has nearly declined. However, trends do not emerge in one week. Yes, we are at a time of year where we traditionally see seasonal declines, but we need to see more.

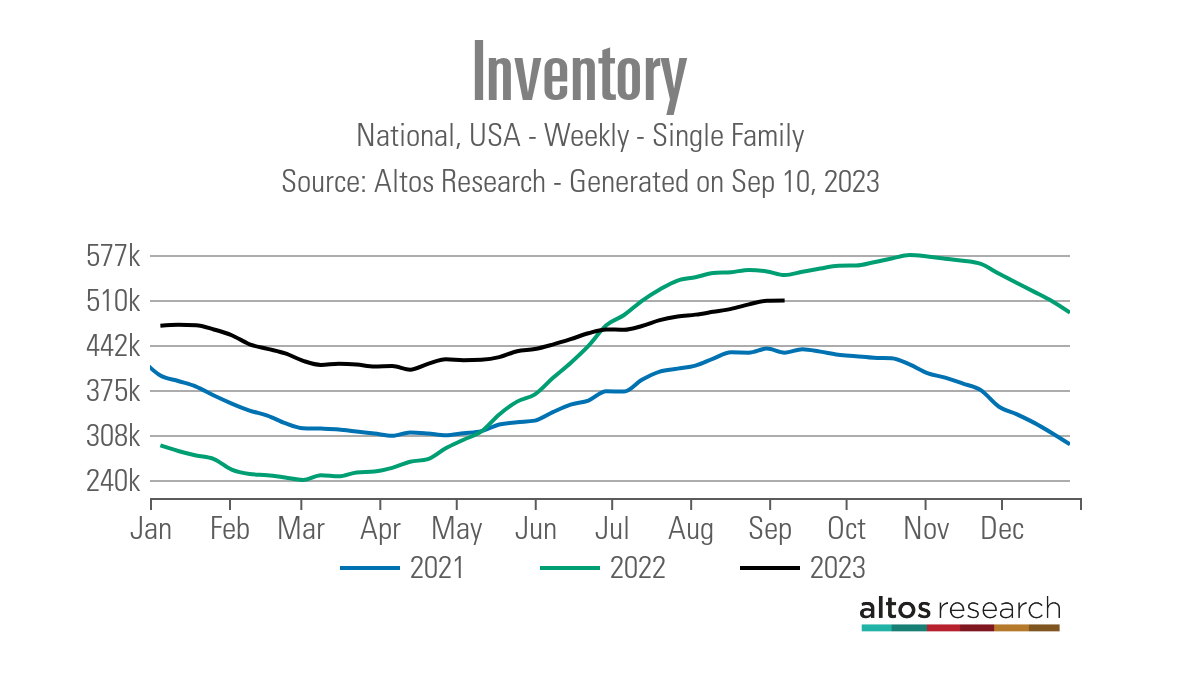

Last year, the number of active listings decreased during the same week, but the number of listings continued to increase until October 28th. But we have to be mindful of comparisons to this year, as home sales are collapsing at the fastest rate in history in 2022. last. That being said, we hope to extend the stock increase further before a seasonal decline occurs. According to , the numbers are: Altos Research:

- Weekly inventory changes (September 1st to September 8th): Inventory has increased 508,813 to 509,156

- Same week of the previous year (September 2nd to September 9th): Inventory decreased compared to the previous year 552,536 to 547,222

- The bottom price of inventory in 2022 is 240,194

- So far, the inventory peaks for 2023 are: 509,156

- Check out this week’s active list for context. 2015 was 1,195,099

Inventory growth has been slow this year, especially compared to last year. This is why I like to tell people to be careful not to read too much into negative year-over-year inventories, as June 2022 inventories are consistently tied to the most significant one-year sales collapse in U.S. history. is.

The new listing data is getting interesting. Two weeks ago, there was a noticeable drop off from trend, but then there was a weekly rebound. I blamed it on the timing of the Labor Day holiday, but last week we saw an even more pronounced week-to-week decline. We hope to see a return to previous trends next week. New listing data from July 21st is as follows.

- July 21st: 63,375

- July 28: 62,525

- August 4: 61,490

- August 11: 60,759

- August 18: 60,295

- August 25th: 55,291

- September 1: 60,004

- September 8: 50,212

After some time of a gradual, orderly seasonal decline, the past three weeks have been eventful.

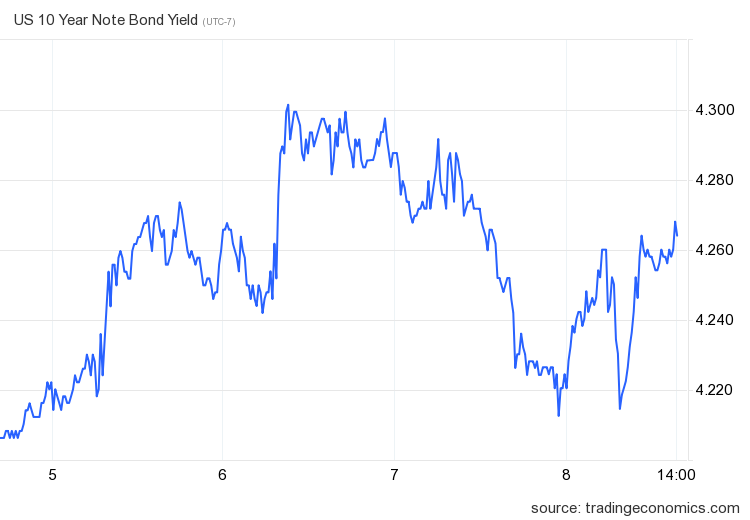

Mortgage interest rates and bond markets

Last week, mortgage rates caught up with rising bond yields and rose to their highest level. 7.33% before the week ends 7.22%.The only significant level for me since beyond my peak 4.25% Will the 10-year yield call be able to break over the 10-year yield? 4.34%, This was the highest intraday price last year.

So far, three attempts to break through that level have been unsuccessful, but I’m betting on it because breaking through that level could send mortgage rates to new highs in 2023. I’m paying attention.

Purchase application data

Purchase request data is down 2% Every week, we create a count from the beginning of the year to the present. 15 positive, 18 minus print and a flat week. Starting on November 9, 2022, 22 positive print vs 18 minus print and A flat week.

Rising interest rates have slowed demand, and purchasing apps have returned to 1995 levels. But we have to remember that the purchasing app is highly seasonal, as the bars are shallow here, the data line is back to 1995 levels, and the total volume always decreases after May. Demand rebounded a bit last year when mortgage rates fell, but context is key. Today we are working from an insufficient level.

Next week: Inflation week again

At this time of the month, two inflation reports are released to give you an idea of the inflation situation: CPI and PPI. Headline inflation has risen recently due to rising oil prices, but there is room for further downward pressure on core inflation.of federal reserve is more concerned about core inflation data, which should be key to this week’s CPI report.

retail sales and Applying for unemployment insurance There are also several important economic reports scheduled to be released this week that could move the bond market. And of course, since these two have been doing a nice slow dance since 1971, that could be moving mortgage rates.