The best way to deal with inflation is to always increase supply. If you’re trying to beat inflation by destroying demand, you’ve already lost the battle and you’re hurting future production. That’s why today’s housing completion data was good news.

During a traditional recession, builders usually show low starts, permits, and completions data. But in a strange twist, builders now have a huge backlog of homes that need to be completed, which is historically an anomaly. This is why construction workers still have jobs and need to complete their backlogs. This is a positive result.

The bigger story here is that if we want lower mortgage rates, we need more units to rent and there is currently a massive backlog of two-unit homes under construction, over 900,000. is. Without a backlog of rental units that need to be built, next year’s inflation story wouldn’t look so rosy.

so the latest national census Reports, home completion data increased. Still, other than that, it’s the classic recessionary sector story I wrote in June. talked at CNBC A few months ago. So let’s take a look at today’s housing starts data.

From the Census: Home Completions Privately owned home completions in November were at a seasonally adjusted annual rate of 1,490,000. This is 10.8% (±15.8%)* above the October revised forecast of 1,345,000 and 6.0% (±17.6%)* above the November 2021 forecast of 1,406,000. The completion rate for single-family homes in November was 1,047,000. This is 9.5% (±12.9%)* above the October revised rate of 956,000. 430,000 units in November for buildings with 5 or more units.

Traditionally, as seen in 2002-2005, housing starts, permits, and completions have been done together. However, slowdowns in the supply chain have made it take too long to build homes in recent years. The upside is that builders will keep construction workers employed and generate more supply to combat inflation next year.

Talking about a housing recession is different from talking about completed houses or remaining inventory. Housing permits are declining because builders need to feel more confident in building something. Cheaper housing is a scary business model because builders need to get paid. So that’s the end of the housing permit story. Builders complete what they are legally required to do. After that process, it’s all about fees, fees, and other fees.

From the Census: Building Permits Privately owned residential units authorized by building permits in November were at a seasonally adjusted annual rate of 1,342,000. This is 11.2% below the October revised rate of 1,512,000 and 22.4% below the November 2021 rate of 1,729,000. November single-family approvals were at a rate of 781,000. This is 7.1% below the October revision of 841,000. Unit approvals for buildings of five or more units in November were at a rate of 509,000.

You can see more evidence of the housing recession in the chart below. Permits are predictably dropping as demand is weakening. From 2002 to 2005, the housing bubble steadily rose and then burst. I know how wild the COVID-19 data was, but when you smoothed out the heated part, it never came close to the output seen during the housing bubble.

We are also doing house construction. Builders have a backlog of orders here, but lower than in the multifamily sector. We should be grateful that the backlog exists.

From the Census: Home Starts Privately owned home starts were at a seasonally adjusted annual rate of 1,427,000 in November. This is 0.5% (±12.3%)* below the October revised forecast of 1,434,000 and 16.4% (±13.4%) below the November 2021 forecast of 1,706,000. Multi-family housing starts totaled 828,000 in November. This is 4.1% (±11.3%)* below the October revised figure of 863,000. Buildings with 5 or more units in November were 584,000 units.

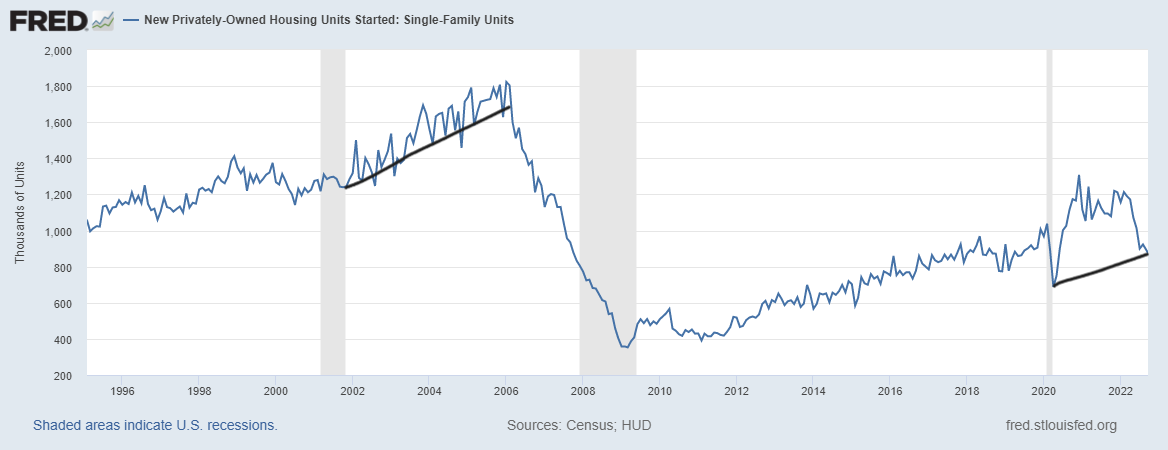

The broadest housing recession data line is single-family starts. As you can see in the chart below, single-family starts are heading towards their low levels with COVID-19. Home builders will not issue new permits to build single-family homes until monthly supply levels drop.

My rule of thumb for predicting builder behavior is based on a 3-month supply average. This has nothing to do with the existing home sales market. This monthly supply data applies only to the new home sales market.

- when supplied 4.3 months, Below are some excellent markets for builders.

- when supplied 4.4-6.4 months, which is an OK market for builders. As long as sales of new homes are growing, they will be built.

- Builders stop building when supplies run out. 6.5 months that’s all.

We currently have 8.9 months of supply and will have an update on this data line next week.

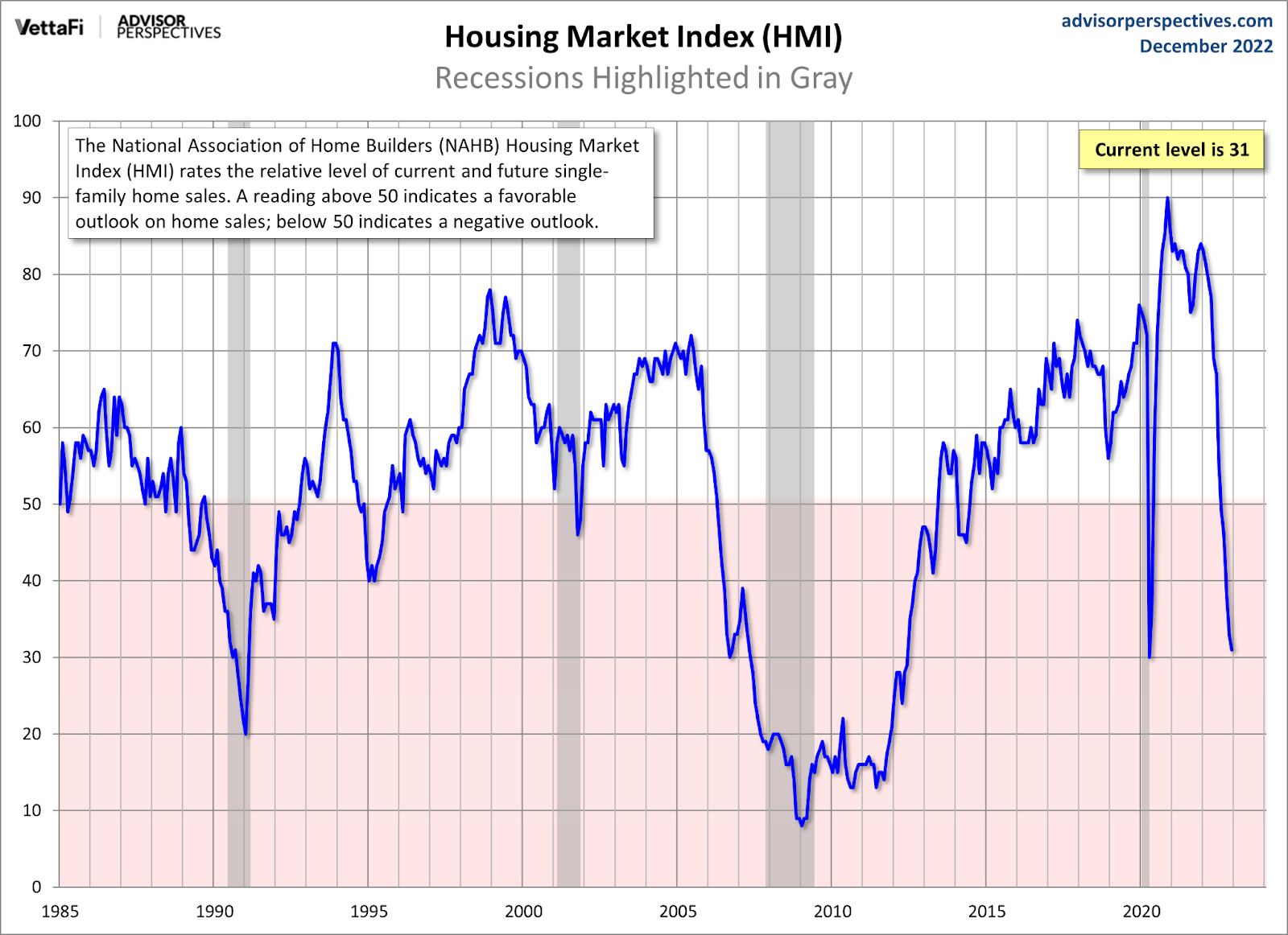

Builder confidence data was released yesterday, but the decline in the index continues. If this situation continues, the housing slump over future housing production outside the backlog of orders will continue.

There was some good news, though. Forward-looking data on sales six months ahead were positive.

from NAHB/Wells Fargo Housing Market Index (HMI): “The silver lining for this HMI report is that the index has seen the smallest decline in the last six months, suggesting that builder sentiment may be nearing the bottom of the cycle. Mortgage rates have fallen to around 6.3% today from over 7% in recent weeks, and for the first time since April, builders recorded a rise in future sales expectations.”

Over the past six weeks, we’ve seen buyers return to the data line when mortgage rates fell from 7.373% to 6.12%. Forward-looking purchase requisition data found a trough at the data line and has been rising ever since. Mortgage rates have risen from recent lows. But this is a good sign that he doesn’t even need to bring interest rates back to 5%. Interest rates need to reach his low 6% range, followed by duration, for the market to stabilize to some degree.

The housing starts report was good because the number of completed homes increased. This is the most positive story about a mortgage rate cut next year. The housing slump that began in June is still ongoing, as evidenced by the collapse of the Builder Confidence Index. The longer this housing recession lasts, the lower productivity will be.

We anticipate a significant slowdown in multifamily construction next year, but our backlog of over 900,000 units under construction is what we should all be rooting for to achieve. Inflation needs to slow down to keep mortgage rates down, and shelter inflation is a big driver of core inflation.