As we wrap up 2022, it’s time to look back at a historic year for the housing market that was even more intense than the 2020 COVID-19 year. There are similarities and significant differences between this year’s housing recession and the 2008 housing recession. , and looking at specific factors in both timeframes gives us an idea of what to expect in 2023.

First, we need to define what a recession is. Our general economy isn’t in recession yet, but housing has been in recession since the summer. For me, it’s plain and simple. That’s when four things happen in every sector of our economy:

1. sales fallDemand for housing has fallen significantly this year.

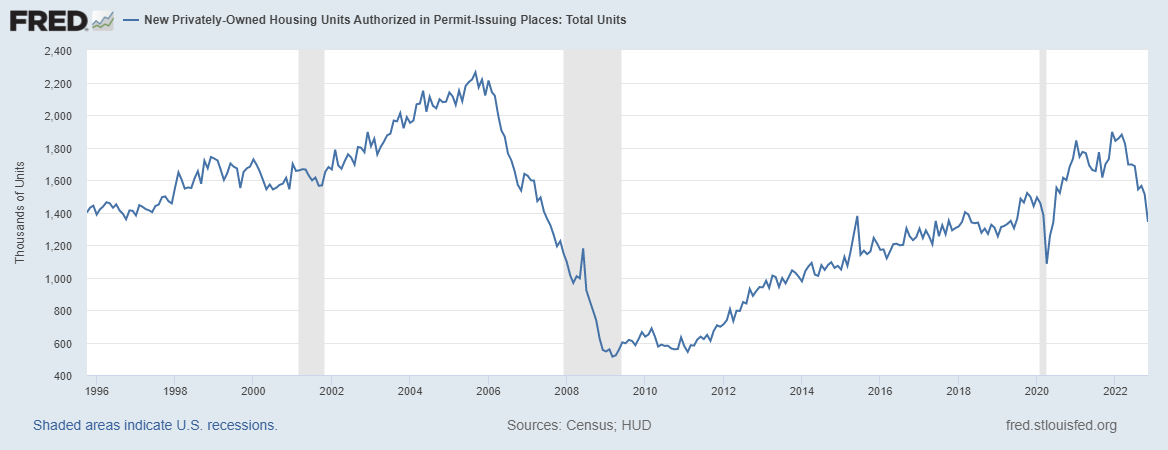

2. production dropsHousing permits and starts are currently declining, despite the backlog of housing in the system.

3. job is lostThe housing sector, especially real estate and mortgages, will see significant job cuts, and the general economy will create more than 4 million jobs in 2022.

Four. decrease in incomeGeneral income in the housing sector is down due to lower transaction volumes.

A few months ago I was asked to continue CNBC And we’ll talk about why we’re calling this the housing recession, and why this year reminds us of 2018, but worse for the four items above.

Given that even in March of this year, the bidding war was accelerating before mortgage rates rose, it’s crazy to think these four things are happening in the housing market. A byproduct of a sector where house prices have gotten out of control since 2020.

Then we had the biggest Mortgage interest rate shock In recent history, though, total home sales this year will exceed 5 million. This debate can sometimes be derailed by people saying housing won’t go into a recession in 2022 because house prices will rise.

This is just the wrong view of housing economics. As shown above, rising house prices have nothing to do with housing being in recession. Housing was in recession in 2006, but prices didn’t collapse that year.

Let’s compare the recession drivers of 2008 and now.

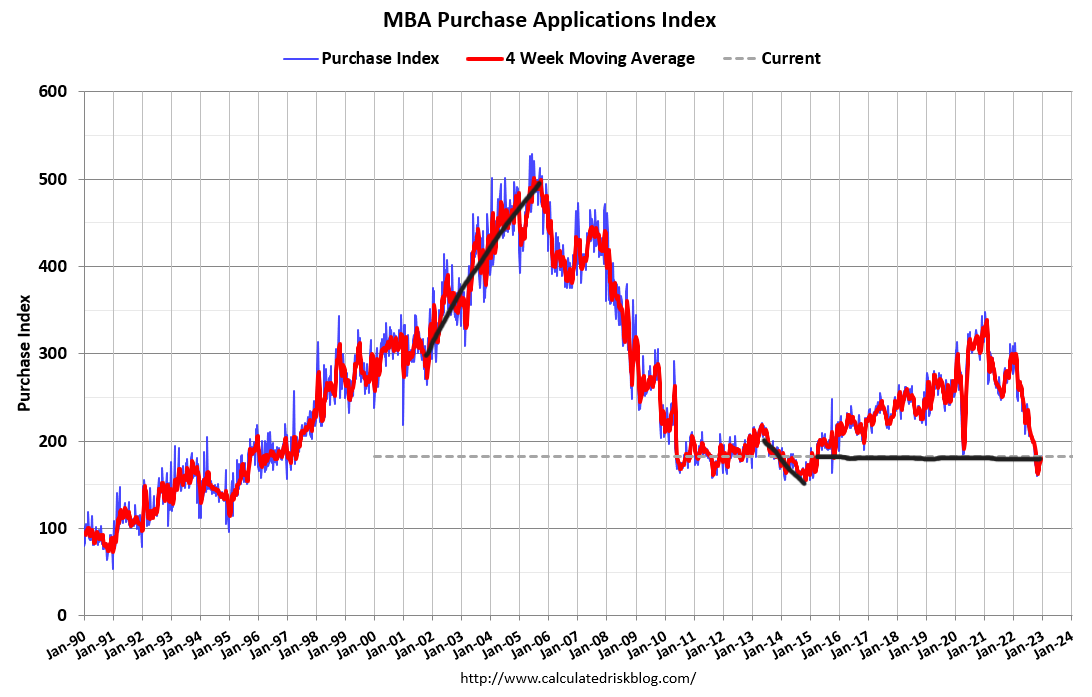

house sales

In the housing market from 2002 to 2005, credit drove four years of sales growth. As shown below, the purchase requisition data he increased for four years, peaked in 2005, and then declined. In the current market, purchase requisition data has recently fallen below 2008 levels.

The difference, however, is that we haven’t had the massive sales boom that we saw in 2002-2005. For his one year only, 2020-2021, purchase requisition data increased. The COVID-19 pause and rebound meant that the end of 2020 was artificially high, so we could argue that we had two years of decent growth, but that’s about it. This is very different from his 2002-2005 period, when credit expansion was booming.

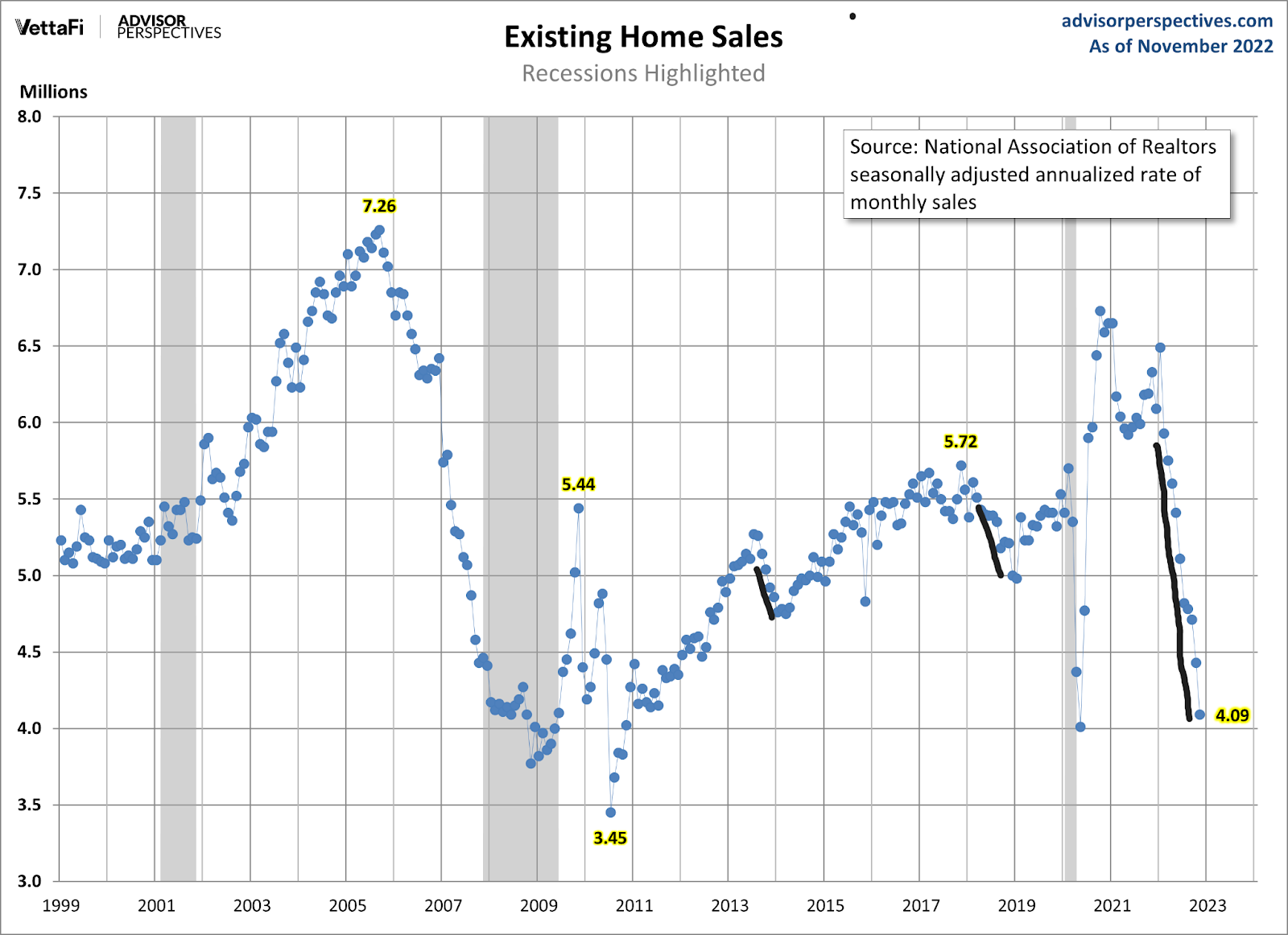

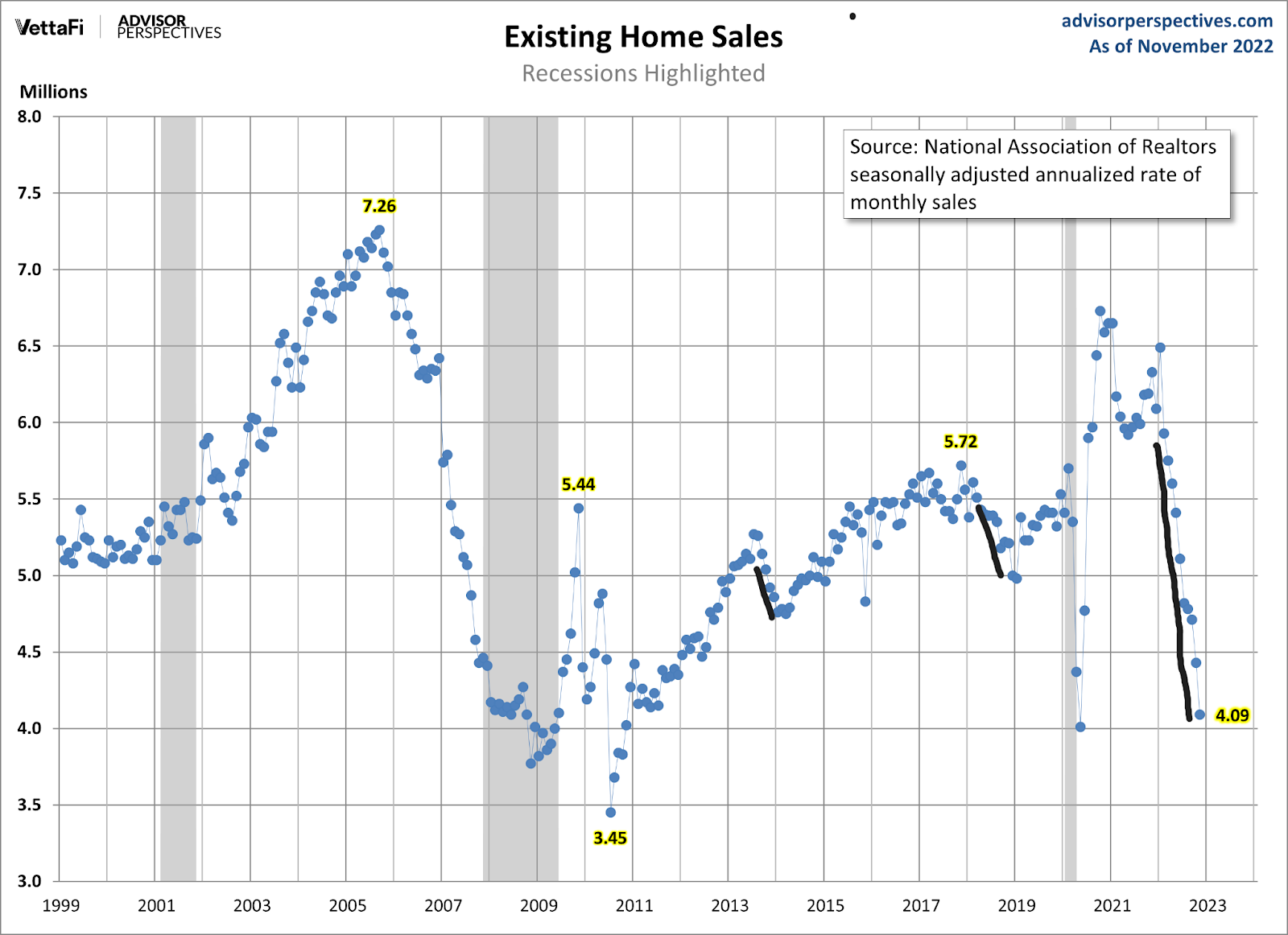

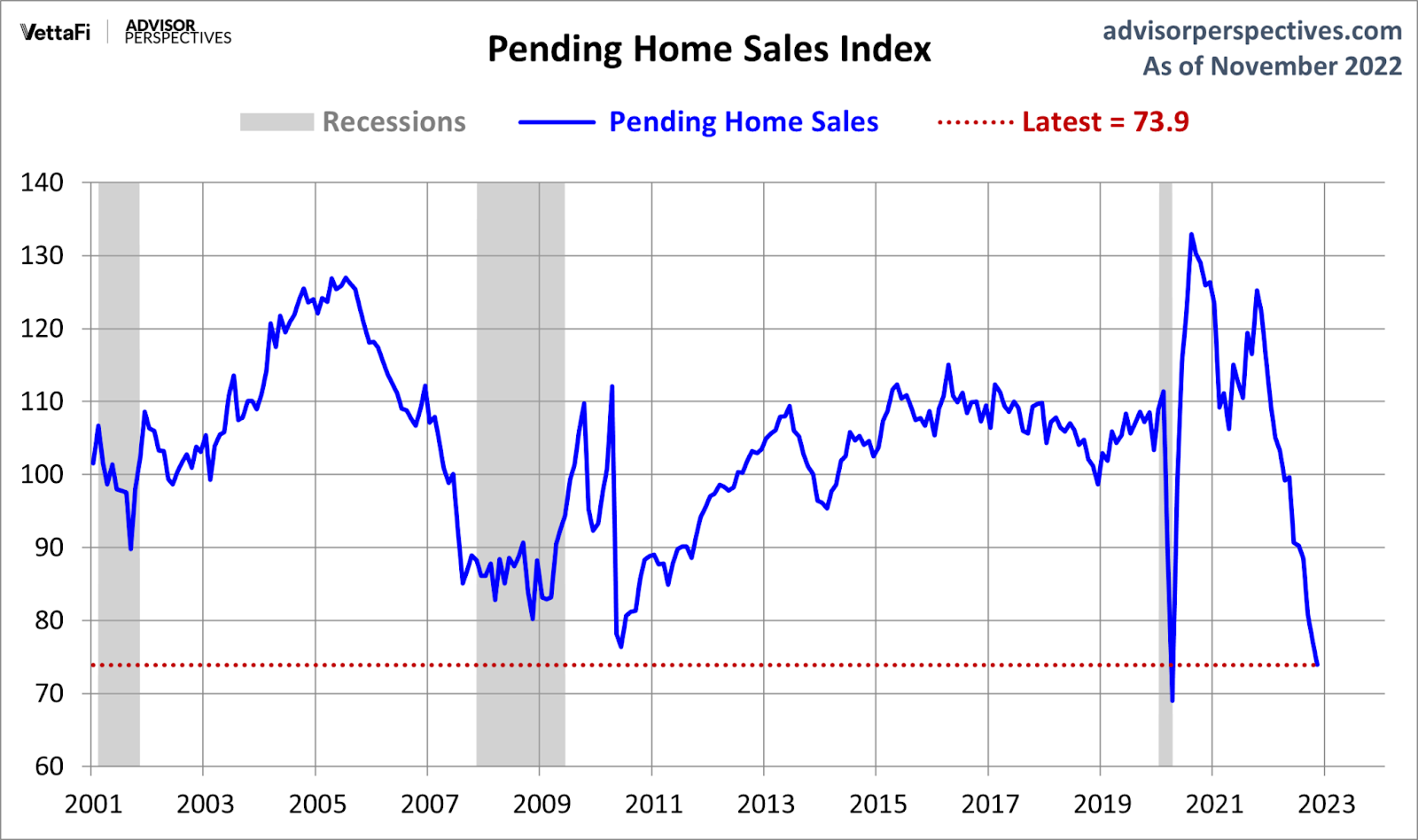

For existing home sales, demand has plummeted like a waterfall, and this happened in less than a year. During the housing bubble, home sales peaked in 2005, and it took him two years to return to current sales levels.As you can see below, previous expansions have had periods of rising interest rates and downward sales trends 5 millionWell, we have one more report to go before the end of the year, so it could go bust. 4 million.

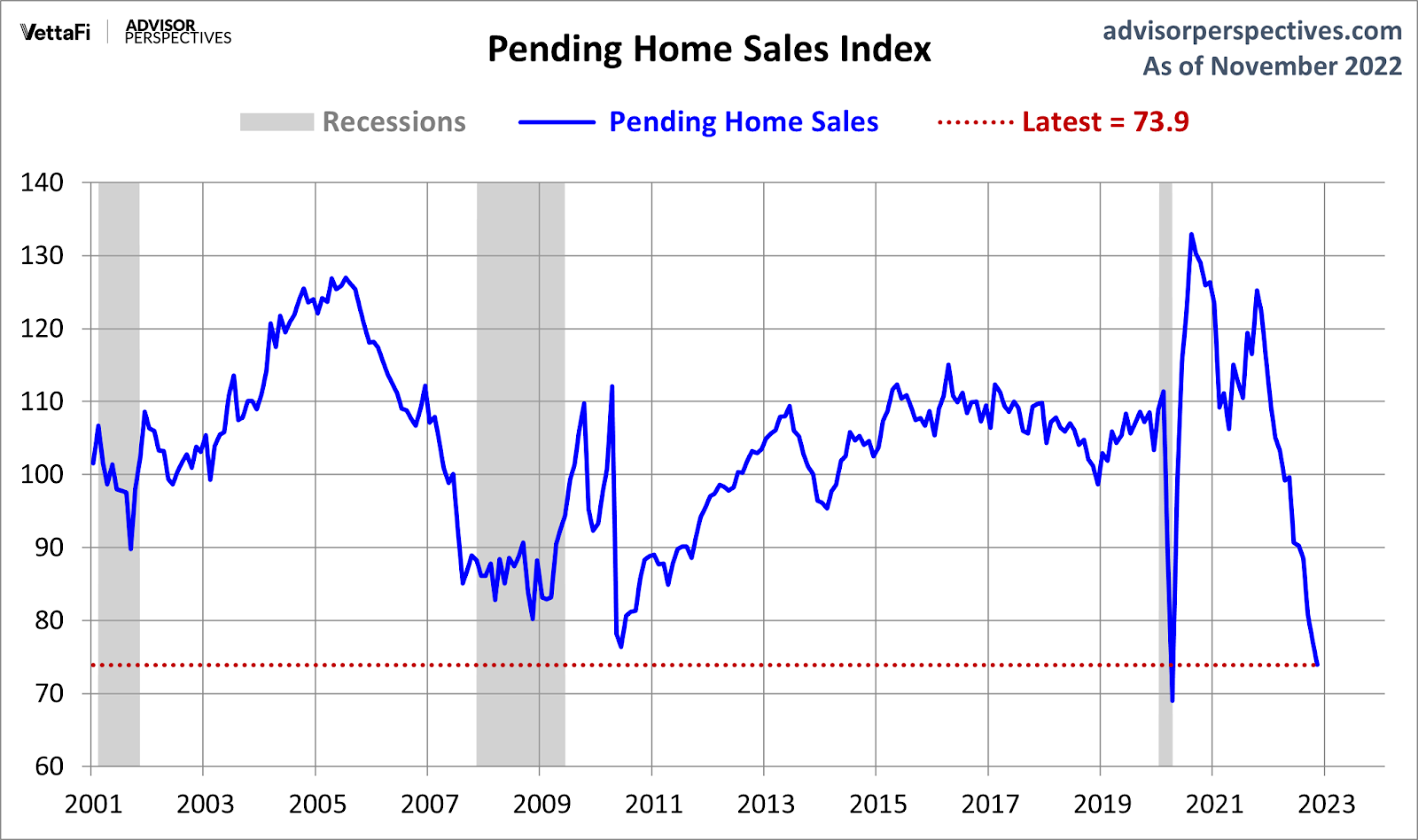

Other than COVID-19, pending home sales have yet to hit a century low. Part of the problem is that mortgage rates have risen so quickly that many sellers have quit again this year.

Important thing to remember: traditional sellers are usually also buyers. This common sense reality has long been lost in discussions of the economics of the housing market. Because people were pushing the false narrative of supply spikes. That means people sell their homes and become homeless. In fact, when traditional primary resident homeowners list their home, they usually buy another.

For some sellers, when mortgage rates soared as they did this year, homes 6.25%-7.37%. This has led to many people not listing their homes for sale, driving a much larger decline in home sales than in the past. We come into one subject, inventory and credit.

housing inventory

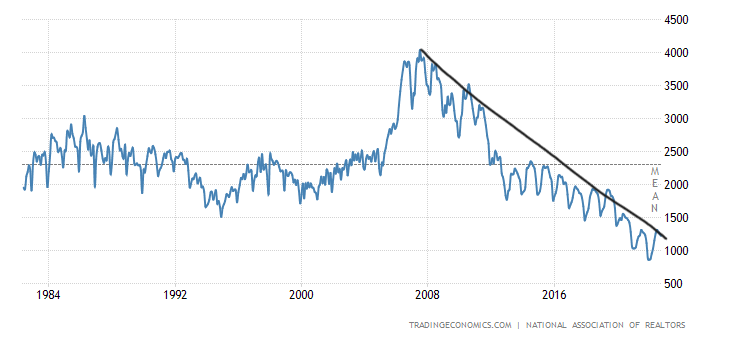

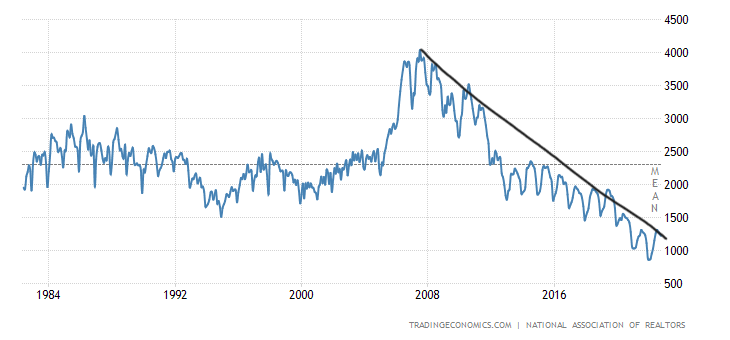

This aspect of the housing market is where we see the biggest difference between 2008 and now.TOTAL HOME INVENTORY TODAY — USING NAR data – Is standing 1.14 million. It’s entirely possible that the total number of active listings in the next two existing home sales reports is less than 1 million. This means 2023 will start with the second lowest level listing in history.

As I explained, this started in 2000 and in 2005 the total number of active listings increased from 2 million to 2.5 million. So when housing peaked in 2005, the flood of inventory from home sellers who couldn’t buy homes caused listings to skyrocket. 4 million in 2007.

As you can see below, today — just days away from 2023 — existing home sales are trending to 2007 sales levels, but they are markedly different.

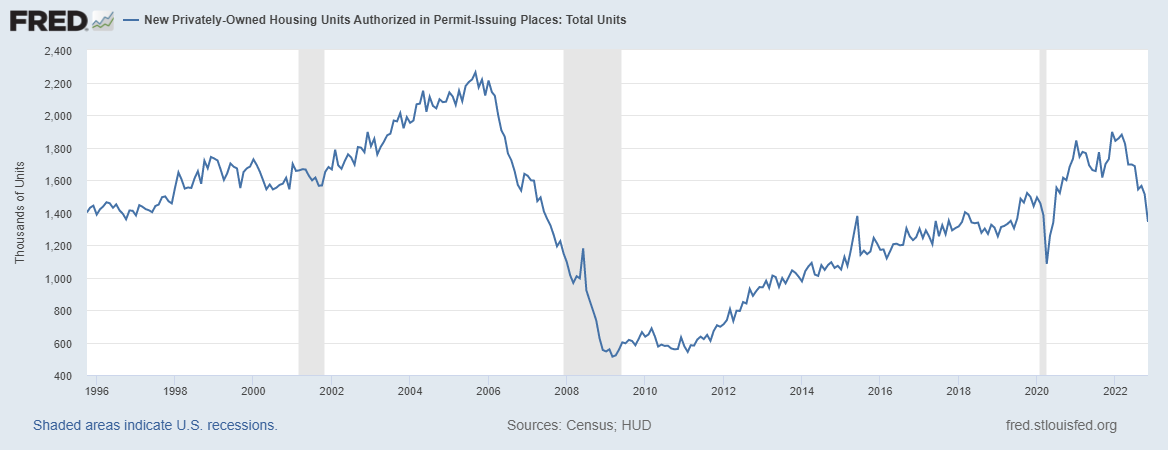

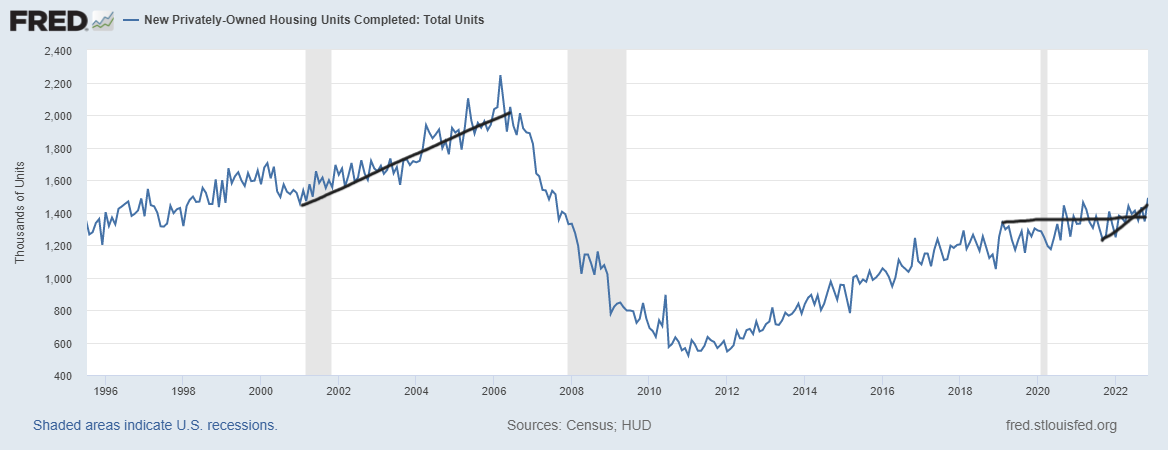

The housing economy is built on housing construction, and the recession that started in June meant a decline in housing permits. The problem is that when the housing recession hit in 2007, supply surged significantly. That is not the case now, and as long as mortgage rates remain high, housing permits may continue to fall.

One saving grace today is that builders still have a huge backlog of homes to build. In particular, the 2-unit rental units will add nearly 1 million in supply online next year. This is a big plus in fighting inflation.

Important things to remember: The best way to combat inflation is to increase supply. If you’re trying to fight inflation by destroying demand, it’s not the most effective means and could ruin future production. This will be a topic of discussion if a housing permit is issued in .

The good news for 2023 is that supply is still coming in, and we should all be rooting for improved home completion data next year. Secondly, although sales are declining, there have been no completions for some time. This is due to the absence of his 2020-2022 credit boom that was seen in 2002-05.

Housing loan

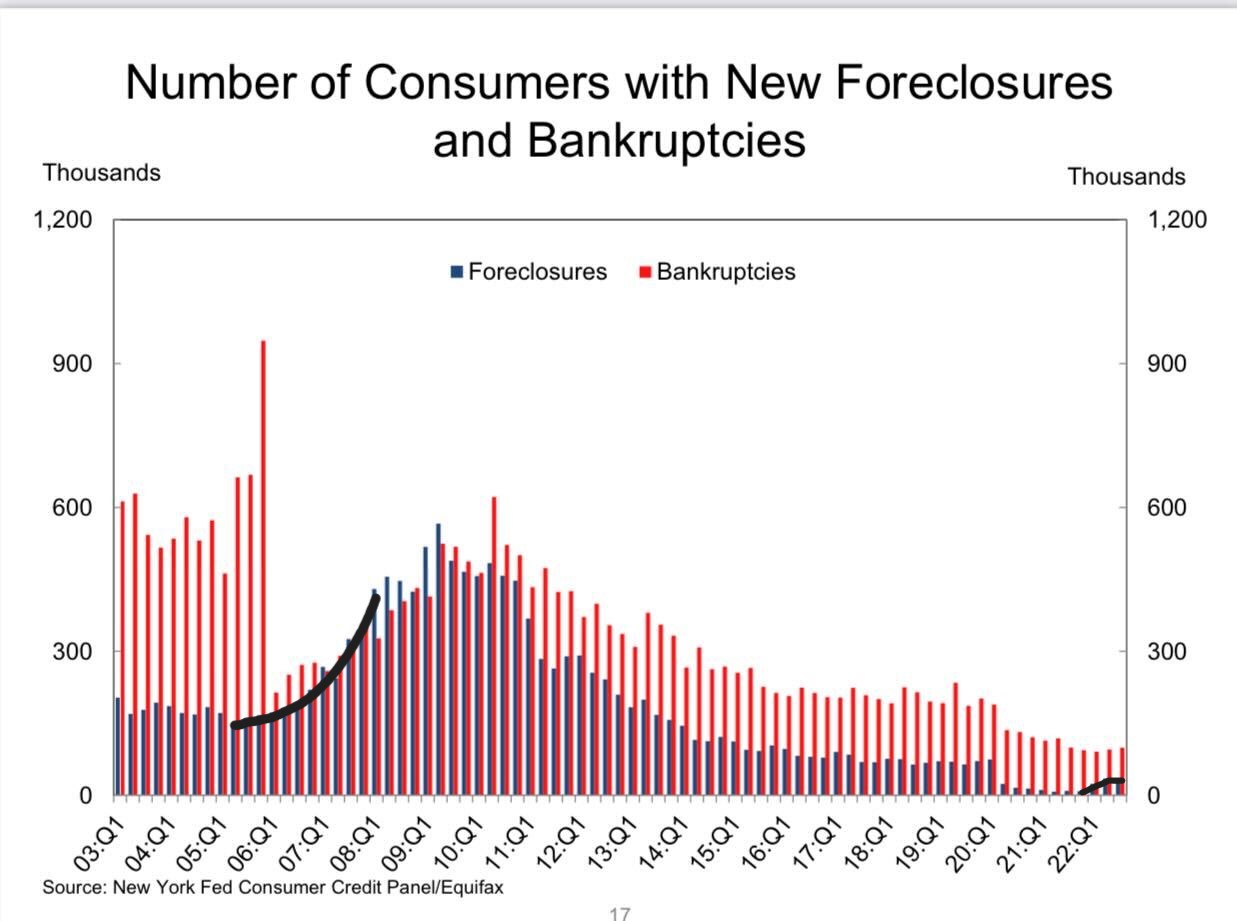

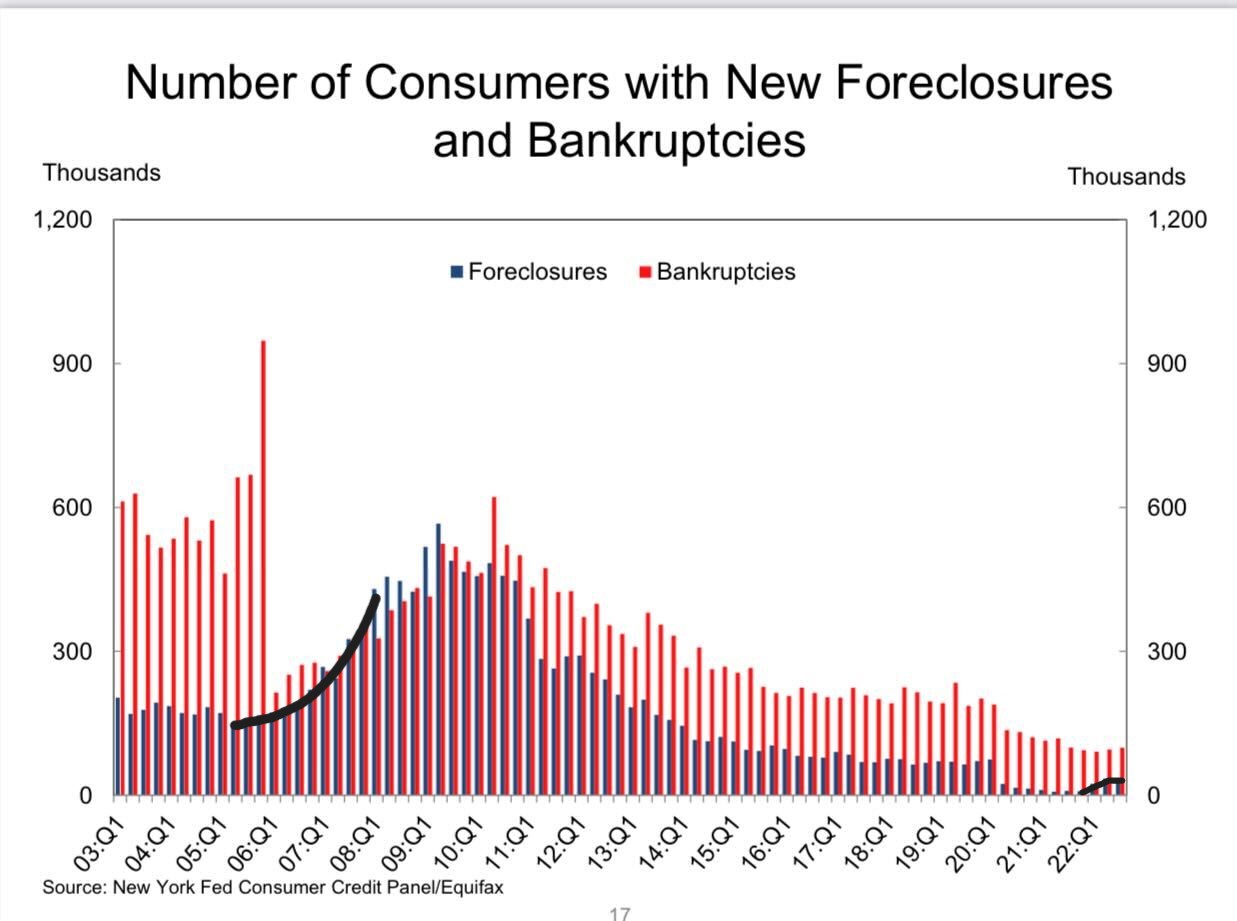

The biggest difference between the current recession and 2008 is mortgages. In 2008, Increase in foreclosures and bankruptcies It was waving red flags before the unemployment recession hit. Today, it’s quite the opposite. The Bankruptcy Reform Act of 2005 and the Qualified Mortgage Act of 2010 laid the foundation for the highest mortgage profile in US history.

From 2005 to 2008 we saw an increase in foreclosures, but that was all before the unemployment recession hit. That’s not what housing credit risk should look like.

There is real credit risk now as prices have fallen from their peaks in some areas. Late-cycle lending risk is always traditional. People who buy homes late in the economic expansion and lose their jobs without selling their shares can lead to foreclosures. FHAMore loan. This means that the size of defaults when the next unemployment recession hits will be smaller than in 2008.

Foreclosures take a long time, traditionally 9 to 12 months. As you can see, when the recession began in 2008, the 90 days lag + foreclosure data line was stretched. But this all really started him in 2005, with new foreclosure and bankruptcy data increasing heading into the 2008 recession.

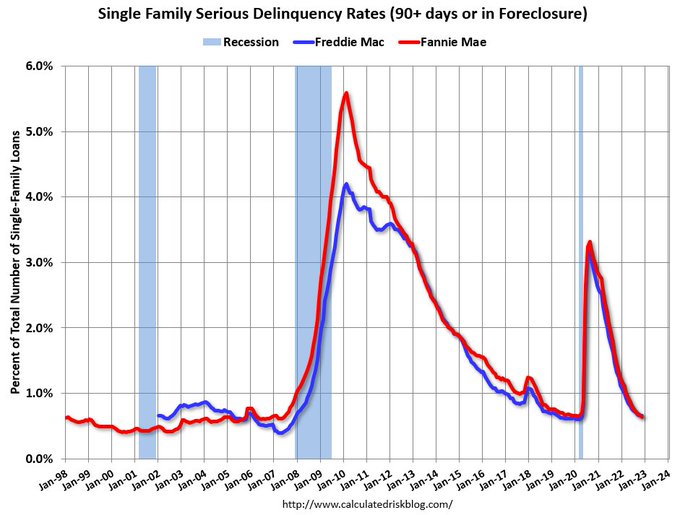

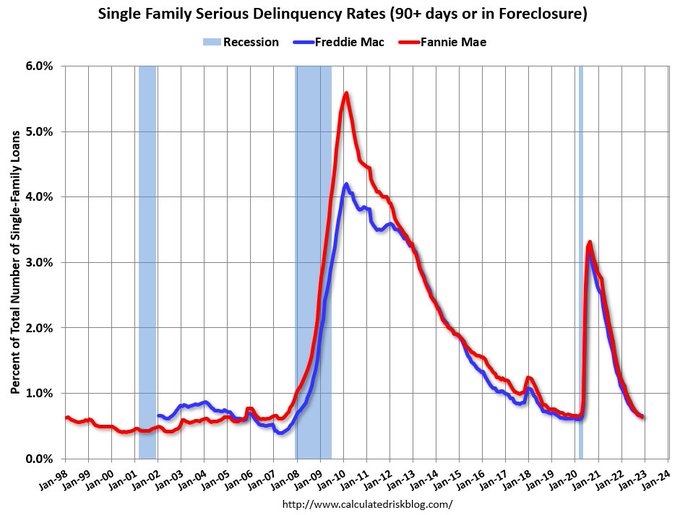

from fannie mae: The traditional single-family home severe delinquency rate fell 3 basis points to 0.64% as of November.

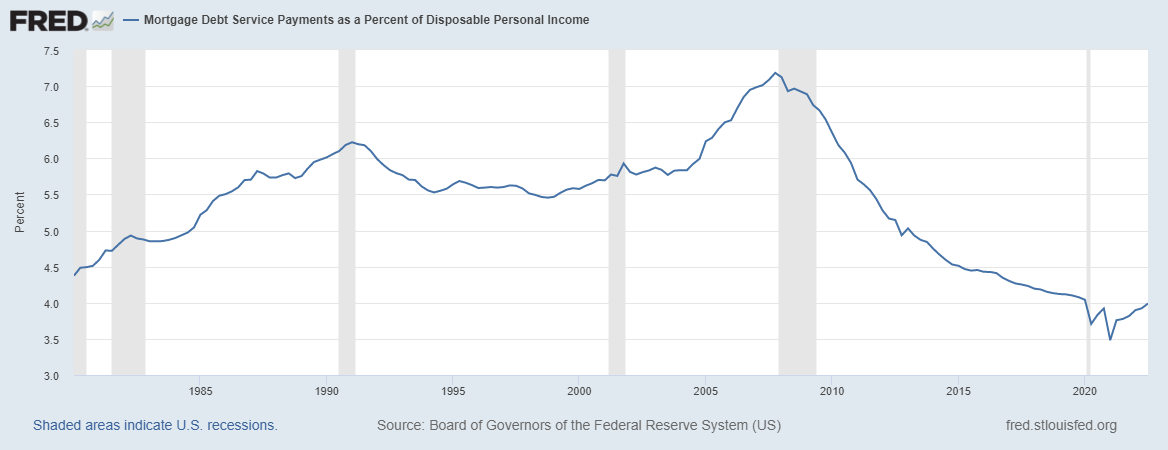

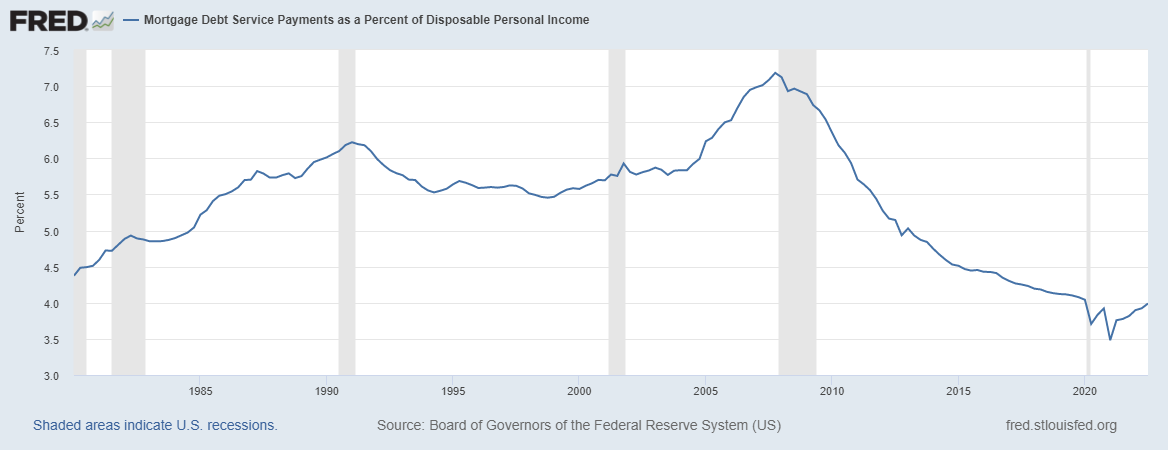

Mortgage review makes mortgage boring again, boring is sexy! Housing is a haven cost to the ability to own debt. That means someone buys a house, debt payments are finalized, wages rise every year, and shelter costs go down while income goes up. This made him one of the most impressive data lines for homeowners.

Mortgage payments as a percentage of disposable personal income are collapsing as people stay home longer. His three refinancings since 2010 have lowered their mortgage costs and gross wages. As you can see below, there is a big difference between the end of 2022 and his end of 2008.

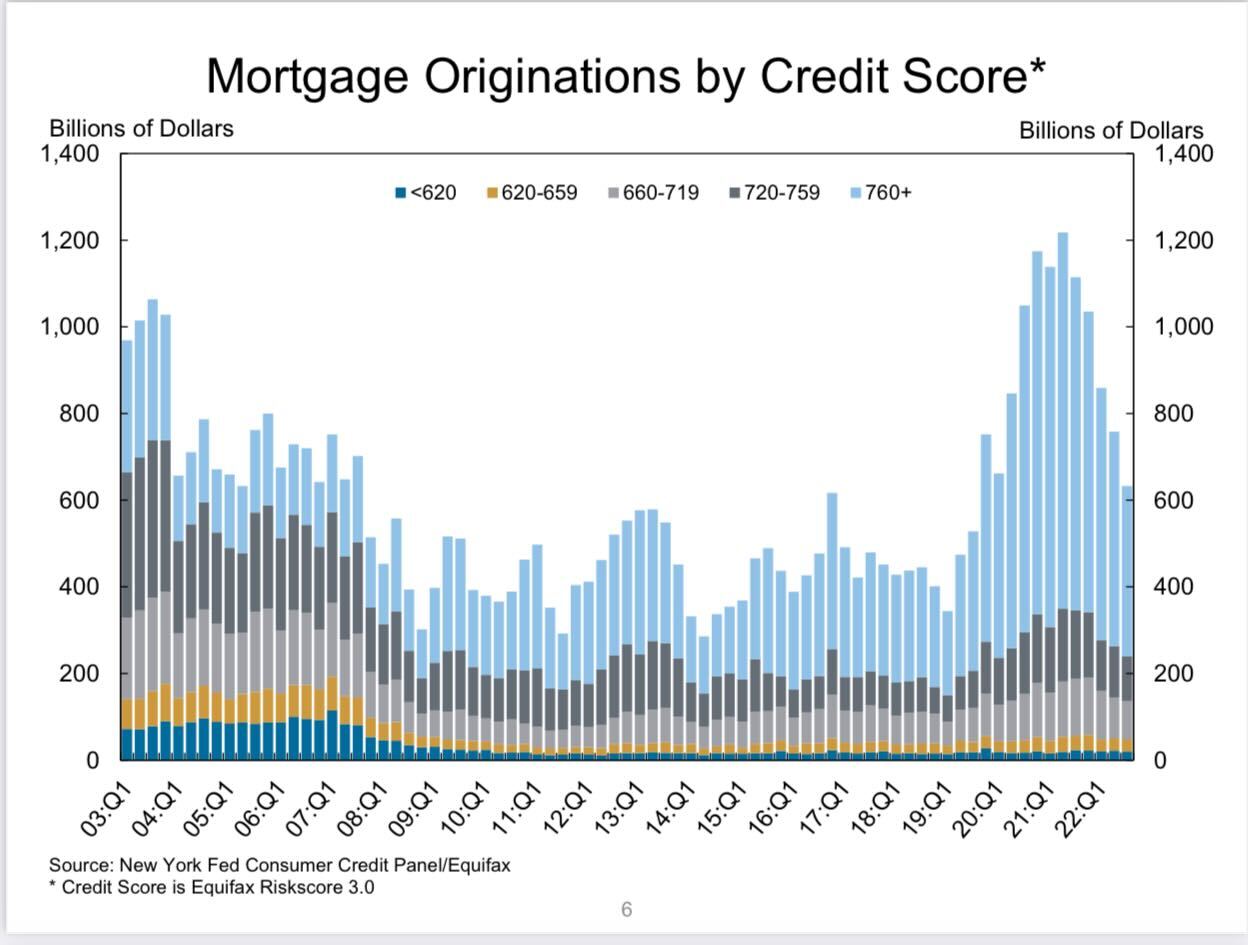

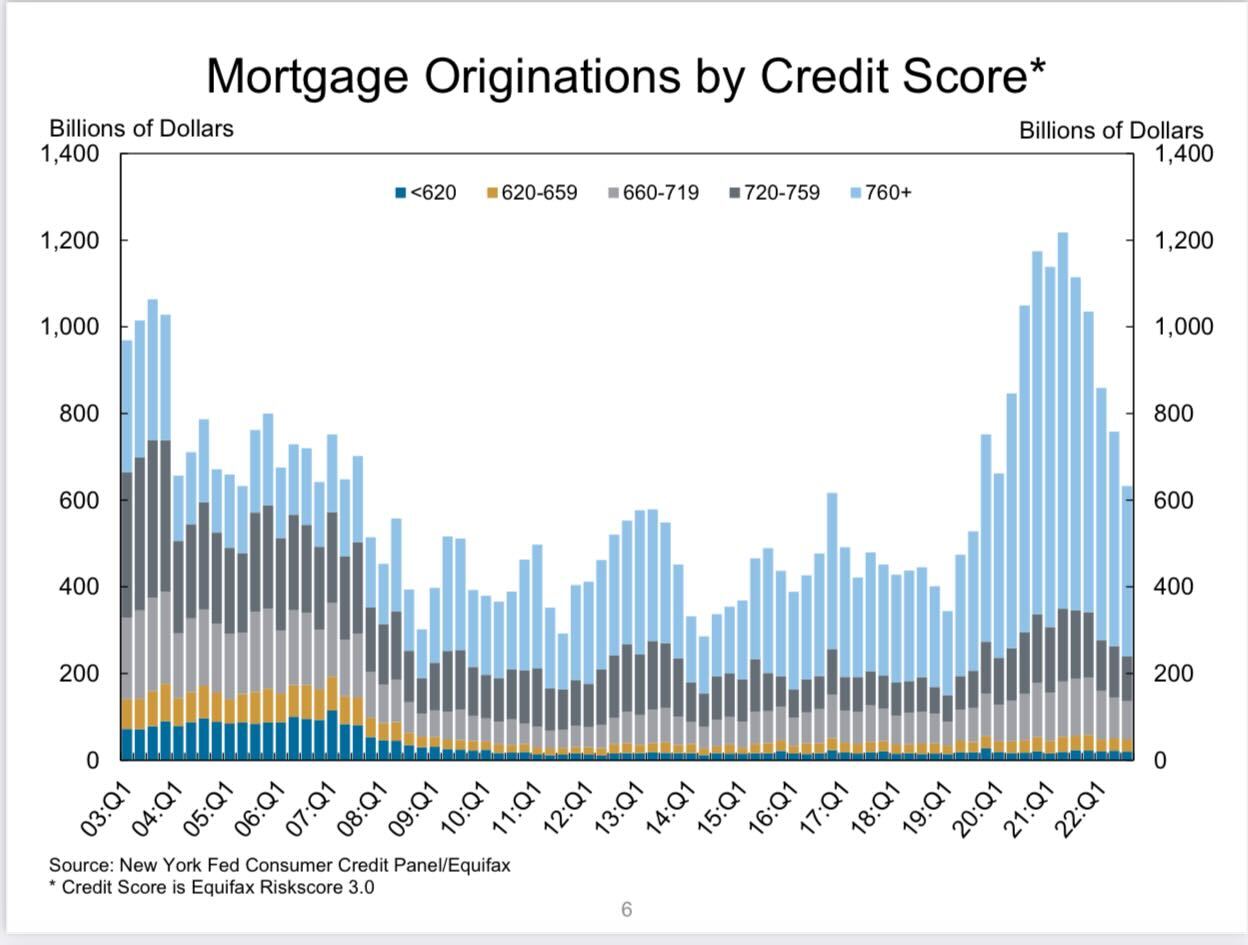

FICO score trend has been stable for 12 years. Some now speculate that the owner’s recent rise in his FICO score is credit he score inflation, but the trend has remained the same for a long time. Just the fact that, as a country, we originated more loans during COVID-19 due to a massive wave of refinancing. People assume this is credit score inflation, but in reality the trend remained the same.

As you can see in the chart below, credit quality is now much better and since 2010 the system has no special loan liability structure.

In addition to homeowner credit looking good, there are many nested stocks and more than 40% of American homes have no mortgage. So, given the balance of credit and debt, the housing market looks very different in this recession.

Inflation-adapted mortgages have not passed the peak of the housing bubble. This is a by-product of the weakest housing recovery in previous expansions. i wrote about this It wasn’t in the 2019 housing bubble, as many claimed before we entered the critical period of 2020-2024.

So is housing in recession? Yes, it is. Around 2008? far cry.

What you’ve shown here can explain why some data look the same and some look very different. This time around, it has taken a more aggressive hit in existing home sales in a faster time. We haven’t seen the surge in inventories that we saw in 2005-2008, nor the crash in the mortgage market.

However, we are in the early stages of housing permits taking a hit and many housing-related jobs have been lost in 2022 due to a decline in demand for housing. The question now is, what about 2023?

Next week I will provide my forecast for 2023. The chaos in today’s housing market data is written in an unprecedented way, while some of the core foundations of housing have held up very well. Happy new year!