The focus is now on underlying inflation. Forget about the energy price collapse that pushed the overall CPI down.

By Wolf Richter of Wolf Street.

Services inflation in the 20 euro-using countries surged to 5.4% in June from a year earlier, up from 5.0% in May, setting a new record for data since 1997, Eurostat said today, confirming preliminary forecasts earlier this month.

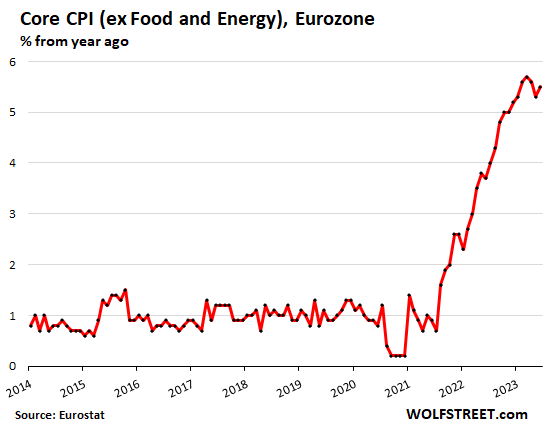

The ‘core’ CPI, which excludes food and energy, climbed to 5.5%, up from a preliminary reading of 5.4% in June and up from 5.3% in May, according to Eurostat. Energy prices have plummeted, and so have food prices, which had been terrifyingly high. But underlying inflation, as measured by core CPI and services CPI, remains a stubborn headache.

The CPI for the service is huge. Once inflation takes hold in the services sector, it is difficult to eliminate. The majority of consumer spending is on services such as healthcare, education, housing, insurance, streaming, subscriptions, airfare, lodging, restaurant dining, repairs, cleaning, financial services and haircuts.

There are many services that are difficult for consumers to compare and consider, some that are essential to modern life such as housing, related services, and healthcare, and others that consumers find it difficult to resist price increases.

“Core” CPI (excluding food and energy) fell to 5.5% in June from a preliminary reading of 5.4%, down from 5.3% in May. It was another nasty inflation surprise, even though core CPI eased slightly in April and May, with experts already declaring a core CPI ‘peak’.

The ECB inflation target is 2%, pegged to core CPI. So this is not going in the right direction.

Back on June 5thWhen May inflation figures were released, with core CPI falling for the second month in a row and experts widely declaring that core CPI had peaked, ECB President Christine Lagarde took a stance against the notion that core CPI had peaked.

“While indicators of underlying inflationary pressures remain high and there are some signs of easing, there is no clear evidence that underlying inflationary pressures have peaked,” he told the European Parliament’s Economic and Monetary Committee.

He also reiterated the ECB’s insistence that it would have to raise rates “to a sufficiently restrictive level” to bring inflation down to the ECB’s 2% target, and that the ECB would maintain those rates “as long as necessary.”

In other words, the “core CPI has peaked” theory, subtitled that no more rate hikes are needed, is now frustrated for the first time.

Overall CPI It has been declining for several months due to plummeting energy prices. CPI nearly halved to 5.5% in June from a peak of 10.6% last October due to soaring energy prices. So overall inflation and core CPI are the same at 5.5%, with core CPI rising and overall CPI plummeting.

And now, the focus is on core and services CPI to get a handle on underlying inflation, which is headed in the wrong direction, with underlying inflation currently above 5%.

No central banker will publicly admit Years of insane money printing and interest rate suppression have fueled this inflationary fire. You may admit it after you leave the central bank, but you won’t admit it while you’re a central banker.

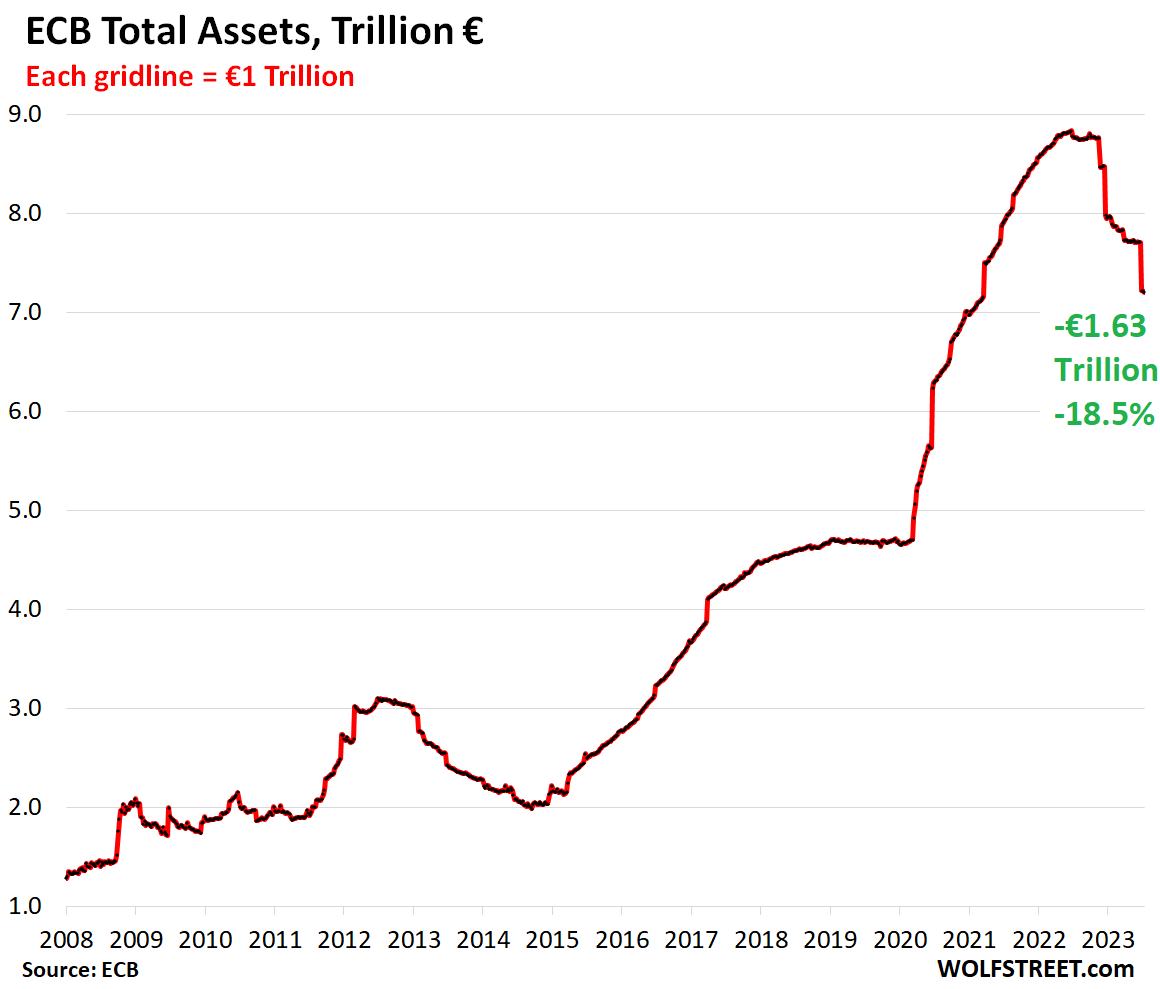

Nevertheless, the ECB has rolled back those factors without acknowledging anything. The policy rate has been raised by 4 percentage points from -0.5% to +3.5% in the past 12 months, and more rate hikes are expected in the future.

And since November last year, it has cut assets on its balance sheet by €1.63 trillion (18.5%) from €8.84 trillion in June to €7.21 trillion as of Tuesday’s balance sheet release. The ECB has now withdrawn 39% of the €4.15 trillion it accumulated during the pandemic. This is a good start.

Read, enjoy, and support Wolf Street? You can donate. I appreciate it very much. Click beer and iced tea mugs to find out how.

Want to be notified by email when new articles are published on WOLFSTREET? Sign up here.

![]()